Emergence of immediate funds transfer as a general-purpose means of payment (16 pages) It is a Chicago Fed paper from Bruce Summers and Kirstin Wells. The main point is that immediate funds transfer needs national programs with support from a central body to succeed in a timely fashion.

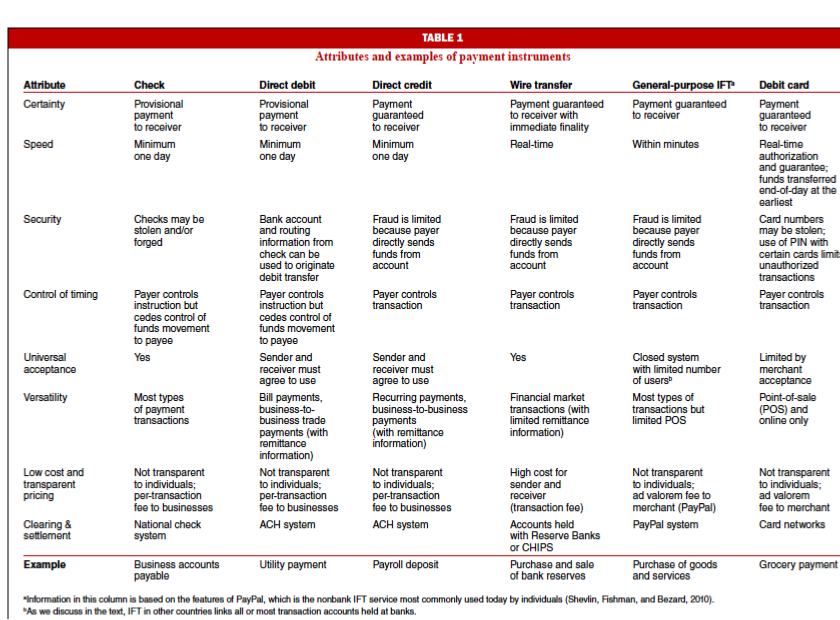

The most advanced means of transferring money between bank accounts is immediate funds transfer (IFT), which allows senders to pay receivers electronically in a highly convenient, certain, and secure manner, at low cost with no or minimal delay in the receivers’ receipt and use of funds.

Today in the United States, IFT payments made through the banking system are mostly limited to large business transactions, interbank transfers, and specialized financial market transactions involving purchases of securities and the like. In total, these larger payments account for a small proportion of the total number of payments made throughout the economy. There is increasing evidence that the popularity of IFT is growing for everyday use, such as consumer purchases, payments between individuals, and small business accounts payable (Hough et al., 2010). To date, however, most general-purpose IFT payments are made on systems operated by nonbanks, the most familiar being PayPal. The coverage of IFT systems supported by nonbank companies is limited to their closed customer groups, and transfers are made not in bank money but rather in special units of account defined by the nonbanks.

This article examines the emergence of IFT as a general-purpose means of payment in the U.S. and in four other countries. We identify the public policy and business issues that arise when a new means of payment is introduced. We describe the attributes of payment instruments that users find attractive and compare the attribute profiles of different kinds of instruments, including IFT. We examine demand for IFT in the U.S. and present four international case studies of IFT. Finally, we discuss barriers to adoption of IFT in the U.S.

Mexico

Immediate funds transfer was introduced in Mexico in 2004, with the implementation of a new RTGS system by Banco de México. The new RTGS system, known by the acronym SPEI, takes advantage of new processing technologies that allow continuous upward scaling of transaction processing volumes at low marginal cost, with strong security based on a public key infrastructure (PKI). During the SPEI project, some commercial banks indicated that they considered two credit transfer systems (the other being the Mexican ACH) to be wasteful. Accordingly, Banco de México designed SPEI to support a variety of credit payments on one processing system, providing banks with a choice between using the new RTGS and ACH. Banco de México has promoted the use of IFT through advertisements in the mass media.

The central bank also provides payment services to the Mexican government and had been using its old RTGS for large government disbursements and the ACH for smaller disbursements.

United Kingdom

Faster Payments is a new IFT service in the UK that makes near-real-time and irrevocable credit transfers available to all bank customers at nonpremium prices. Introduced in May 2008, Faster Payments is available across the banking industry and is supported by common rules and a shared processing infrastructure. Faster Payments is a voluntary initiative of the banking industry, agreed to by the Payment System Task Force, which was organized and chaired by the UK’s Office of Fair Trading (OFT).

Switzerland

Today, IFT is available to businesses and individuals as an extension of the traditional credit slip. In addition to the traditional paper method, IFT is available through Internet banking and ATMs. To illustrate the payer experience with IFT, imagine a computer terminal securely connected to a bank or PostFinance

(the Swiss Post’s financial institution) website. The payer clicks on “making payments” and receives a menu of choices among different types of credit slips, for example, payments to accounts at the same bank, at a different bank, payments with or without reference numbers, and so on.

South Africa

Commercial banks in South Africa identified the need for a payment instrument that would give the general public the ability to transfer funds quickly and in a manner that made funds available to the payee immediately. Seven banks began collaborating in 2005 to develop a new clearing and settlement mechanism called Real-Time Clearing (RTC), in cooperation with the South African Reserve Bank, and the capability was implemented in March 2007.

Conclusion

There is latent demand for IFT in the U.S. by individuals, businesses, and governments, but to date this demand is being met only to a limited extent and principally by nonbank providers of payment services. To satisfy the demand for IFT, it will be necessary to provide access to money held in banks by linking all bank deposit accounts through an immediate if not real-time clearing and settlement system.

The most critical enabling factor is strong sponsorship by a national body with the responsibility and motivation to stimulate continuous improvement in the national payment system. This body might be a consortium of private banks collaborating through a national payment association, a public authority such as the central bank, or a public–private partnership. It is not clear that such sponsorship can be readily found in the U.S., at least not at the present time, because there is no national body that takes responsibility for the development of the national payment system.

If you liked this article, please give it a quick review on ycombinator or StumbleUpon. Thanks

Brian Wang is a Futurist Thought Leader and a popular Science blogger with 1 million readers per month. His blog Nextbigfuture.com is ranked #1 Science News Blog. It covers many disruptive technology and trends including Space, Robotics, Artificial Intelligence, Medicine, Anti-aging Biotechnology, and Nanotechnology.

Known for identifying cutting edge technologies, he is currently a Co-Founder of a startup and fundraiser for high potential early-stage companies. He is the Head of Research for Allocations for deep technology investments and an Angel Investor at Space Angels.

A frequent speaker at corporations, he has been a TEDx speaker, a Singularity University speaker and guest at numerous interviews for radio and podcasts. He is open to public speaking and advising engagements.