Australia’s Resources and Energy Quarterly (March 2012 Quarterly, 182 pages forecasts the world economy and energy out to 2017.

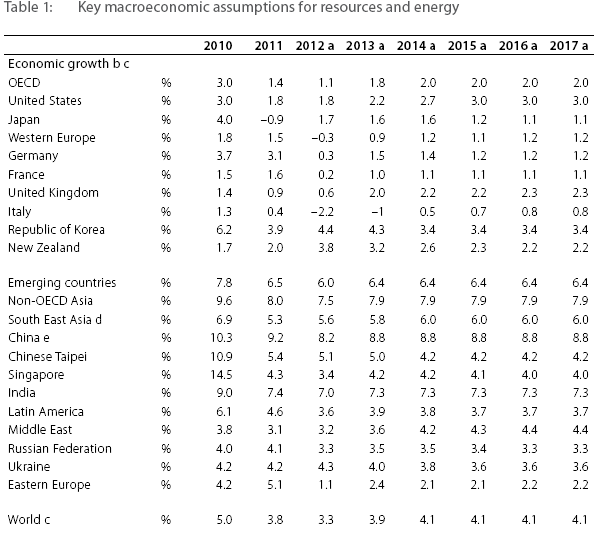

The world economy has entered a challenging period with increased vulnerabilities and a moderation of global growth in 2012 relative to 2010 and 2011. Global economic growth in 2012 is assumed to be around 3.3 per cent (see Figure 1), which is 0.75 percentage points down from the forecast in the September 2011 World Economic Outlook (WEO) by the IMF. The expected slower growth rate is attributed largely to intensifying strains in the euro zone and economic fragilities in some other large economies. Within most of Western Europe short- to medium-term economic growth prospects have diminished. Despite a strengthening of economic activity in the US, global growth and world trade have slowed

China Forecast

The Chinese economy continues to record strong growth, although this is projected to moderate in 2012. In part, this expected easing in economic growth is due to domestic economic policies to combat inflation, including the continuing unwinding of the 2008–09 fiscal stimulus, tighter monetary policy and measures to contain price increases in its property market. Additionally, spillovers from problems in the broader global economy and some high internal risks facing the Chinese economy could threaten and slow economic growth. Internally, socioeconomic factors, such as the structural effect of the so-called ‘middle income trap’, if not well managed, and rising inequality could slow economic growth.

Despite some moderation in economic growth, domestic demand remains strong. Retail sales continue to expand and passenger vehicle sales are just below their late 2010 peak level. Although there has been relatively weaker export demand, manufacturing investment continues to grow. Industrial production growth remains robust, but slightly below 2011 levels, and both power generation and automobile production are growing strongly. As a result, over the outlook period China is expected to continue its major role as a growth engine for the world economy.

For Australia, China is the most important market for mining. Over the medium term, China is expected to remain the most important mining export market for Australia, given a strong trend of continued growth in industrialisation and urbanisation, both of which are resource-intensive.

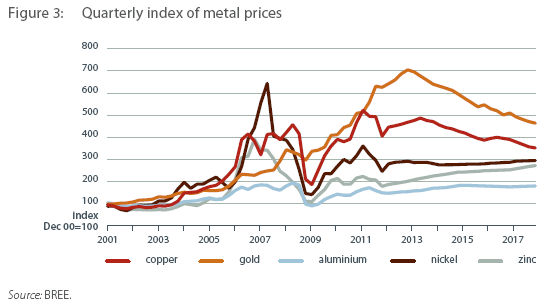

Metal Prices are projected to have a midterm peak in 2013

Oil

The West Texas Intermediate (WTI) oil price is forecast to increase to an average of US$113 a barrel in 2013, assuming crude oil stocks in Cushing return to historic levels. The Brent oil price is forecast to increase to an average of US$119 a barrel in 2013, supported by strong demand from emerging economies. Over the medium term, further increases in oil prices are projected to be limited by higher OPEC spare production capacity and the exploitation of unconventional oil resources. In 2017, the WTI oil price and the Brent oil price are projected to average US$105 and US$104 (in 2012 dollars), respectively.

• World oil consumption is forecast to increase in 2012 and 2013 by 0.9 and 1.4 per cent, respectively. Stronger consumption growth in 2013 reflects assumed improvements in world economic activity. For the remainder of the outlook period, world oil consumption is projected to increase at an average annual rate of 1.1 per cent, as the intensity of oil use within non-OECD economies falls.

World oil consumption is forecast to increase marginally in 2012, reflecting an assumed weak world economic outlook. Beyond 2012, world economic growth is assumed to strengthen. In 2013, world oil consumption is forecast to increase by 1.4 per cent, with oil consumption in non-OECD economies surpassing consumption in the OECD. Over the remainder of the outlook period (2014 to 2017), world oil consumption is projected to increase at an average rate of 1.1 per cent a year, to reach 95.4 million barrels a day in 2017. Increases in world consumption are projected to be characterised by moderating oil consumption growth in non-OECD economies and continuing falls in OECD consumption.

In 2012 and 2013, China’s oil consumption growth is forecast to grow by 4 per cent and 5 per cent, respectively, to reach 10.4 million barrels a day in 2013. China’s oil consumption is projected to increase at an average annual rate of 4 per cent from 2014 to total 12.3 million barrels a day in 2017.

Oil consumption in India is projected to increase by an average annual rate of 3 per cent to be 4.2 million barrels a day by 2017. Projected growth in oil consumption is underpinned by a young population demographic and a growing middle class. Over the medium term, India’s working age population is expected to expand by an average of 1.6 per cent a year and support demand for consumption of petroleum fuels for transport.

Libyan crude oil production is projected to slow and reach 1.9 million barrels a day in 2017.

Official Iraqi oil production targets are ambitious at 6.5 million barrel a day by 2015 and 12 million barrels a day by 2017. Export infrastructure and logistical constraints are likely to limit output growth to below official targets. Between 2014 and 2017, Iraq’s oil production growth is projected to increase at an average annual rate of 6 per cent to reach 4.3 million barrels a day in 2017.

Coal

Over the outlook period world thermal coal imports are projected to increase at an average rate of 4 per cent a year to reach 1040 million tonnes by 2017. The majority of growth is projected to occur in Asia, underpinned by strong import growth in non-OECD Asia, particularly China and India.

Gas, nuclear and renewable electricity generation is expected to increase throughout non-OECD Asia, however, it will still only account for a relatively small share of the total electricity generation in 2017.

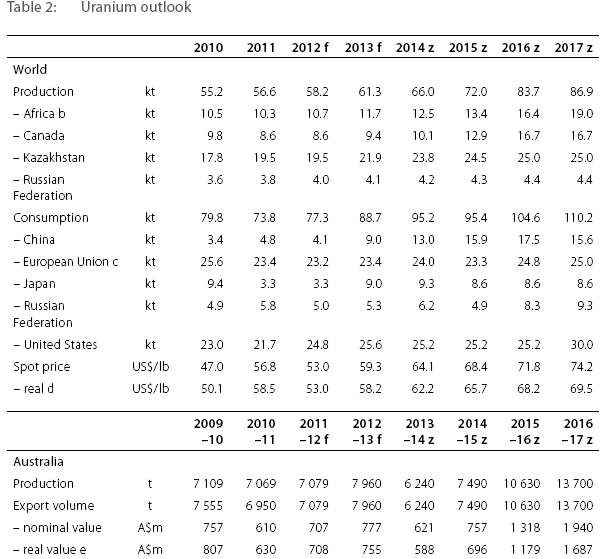

Uranium

• In the short term, the uranium price is forecast to stabilise with lower planned production in Kazakhstan and continued demand growth in developing economies expected to offset lower consumption from reactor closures in Japan and Germany.

• The future of the Japanese nuclear energy industry remains uncertain. It is expected that some nuclear reactors will restart this year; however policy changes that promote decreased reliance on nuclear power in the medium to long term may affect growth in Japan’s uranium consumption.

• Over the outlook period, strong consumption growth from a large number of new reactors starting up, particularly in China, India and the Russian Federation, and reduced supplies from secondary sources are projected to lead to a price increase.

• Increased production from new mining projects and higher export prices are projected to lead to strong growth in Australia’s uranium exports over the outlook period.

The main contributor to growth in world uranium consumption over the medium term will be China. China’s consumption is projected to more than triple between 2011 and 2017 to around 15 500 tonnes, supported by an increase in the number of reactors from 15 in 2011 to around 60 in 2017.

In Asia (including India, but not Japan and China) uranium consumption in 2012 is forecast to increase by 32 per cent to 10 200 tonnes, supported by five new reactors that are expected to commence operation. This includes two in each of India and Chinese Taipei and one in the Republic of Korea.

Over the outlook period, consumption in Asia is projected to increase to around 13 200 tonnes at an average rate of 9 per cent a year. Between 2012 and 2017, a total of 20 new reactors are scheduled to commence operation, including 10 new reactors in India and six in the Republic of Korea.

In 2011, world uranium mine production increased by 2 per cent to around 56 600 tonnes with increases in Kazakhstan offsetting lower output in Canada. For 2012, production is forecast to increase by 3 per cent to approximately 58 200 tonnes as a result of higher Australian and African mine output.

Over the outlook period, world uranium production is projected to increase at an average annual rate of 7 per cent to around 87 000 tonnes in 2017. The production increase is projected to be supported by new mine developments and expansions in Kazakhstan, Africa, Canada and Australia that are in the ramp up phase of production or are already under construction.

Over the medium term, uranium production in Africa is projected to grow at an average rate of 7 per cent a year to around 19000 tonnes in 2017. This growth is expected to be underpinned by the start up of new mines, including AREVA’s Imouraren mine (annual capacity of 2000 tonnes U3O8) in Niger, Extract Resources’ Rössing South (annual capacity of 2300 tonnes U3O8) Trekkopje (1900 tonnes U3O8) in Namibia and Simmer’s Buffelsfontein (annual capacity of 230 tonnes U3O8) in South Africa. An extension to the Rössing mine in Namibia is also expected to increase output by 600 tonnes a year from 2012.

Canada’s uranium production is forecast to remain steady in 2012 after the closure of the 1500 tonne capacity McClean Lake mine resulted in a 12 per cent decrease in production in 2011. Over 2012 to 2017, production is projected to increase at an average rate of 11 per cent a year to reach 16 700 tonnes by 2017. The start up of Cameco’s 4000 tonne a year Cigar Lake mine in 2013 is expected to underpin this growth. Production at the Cigar Lake mine has been delayed several times by flooding, but it is expected to become the world’s second largest uranium mine by 2017. Uranium production in Canada will be further boosted by an expansion at Cameco’s McArthur River mine in 2016 that will increase production by around 1000 tonnes a year.

Australia’s uranium mine production in 2011–12 is forecast to remain constant at around 7100 tonnes. As in 2010-11, production at ERA’s Ranger mine was affected by heavy rainfall in December 2011 and normal operation is not expected to resume until the second half of 2012. Uranium One’s Honeymoon mine in South Australia commenced production in 2011, however, output is forecast to remain low for the remainder of the 2011–12 financial year.

Out to 2016–17, Australia’s uranium mine production is projected to increase at an average rate of 12 per cent a year to 13 500 tonnes in 2016–17. The increase in production is based on the assumption that a number of new mines commence operation within the outlook period. Mines scheduled to start up within the medium term include Toro Energy’s Wiluna operation (annual capacity of 800 tonnes U3O8), Energy and Metals Australia’s Mulga Rocks operation (1200 tonnes U3O8), Mega Uranium’s Lake Maitland mine (1000 tonnes U3O8) and BHP Billiton’s Yeelirrie operation (3500 tonnes U3O8) in Western Australia, and Energy Metals’ Bigrlyi mine

(600 tonnes U3O8) in the Northern Territory. Plans to expand production at BHP Billiton’s Olympic Dam mine in South Australian are not included in this projection as the expansion is not expected to be completed within the outlook period.A number of the above projects are yet to receive company or government approvals and are undergoing feasibility and/or environmental studies. As a result, there is some uncertainty around project capacities and schedules that could result in actual production deviating from projections.

If you liked this article, please give it a quick review on ycombinator or StumbleUpon. Thanks

Brian Wang is a Futurist Thought Leader and a popular Science blogger with 1 million readers per month. His blog Nextbigfuture.com is ranked #1 Science News Blog. It covers many disruptive technology and trends including Space, Robotics, Artificial Intelligence, Medicine, Anti-aging Biotechnology, and Nanotechnology.

Known for identifying cutting edge technologies, he is currently a Co-Founder of a startup and fundraiser for high potential early-stage companies. He is the Head of Research for Allocations for deep technology investments and an Angel Investor at Space Angels.

A frequent speaker at corporations, he has been a TEDx speaker, a Singularity University speaker and guest at numerous interviews for radio and podcasts. He is open to public speaking and advising engagements.