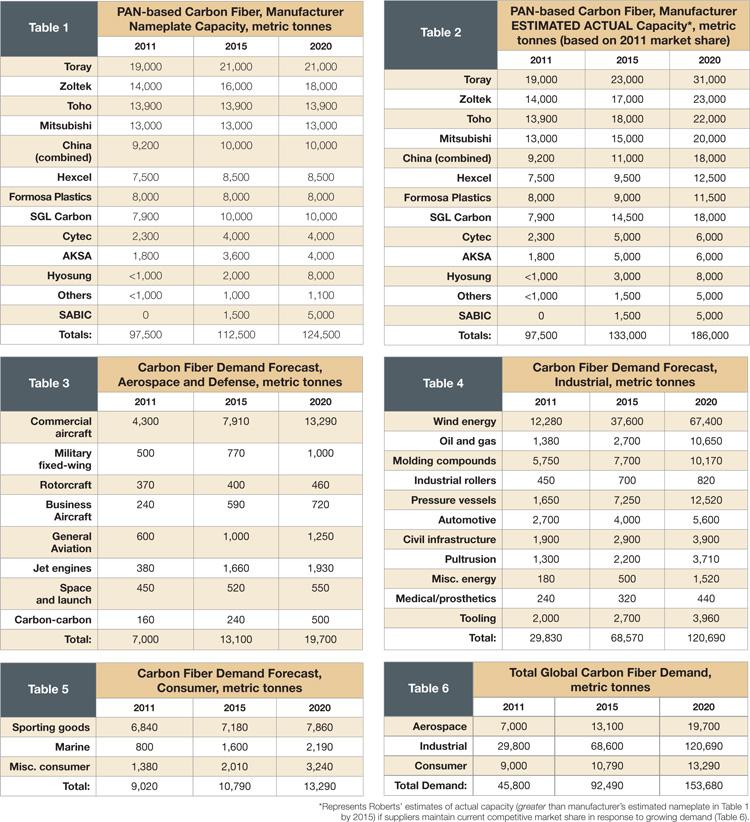

On the supply side, there have been several new entrants since the 2010 conference, including Hyosung (Gyeonggi-do, South Korea), that are on course to manufacture 8,000 metric tonnes (17.637 million lb) by 2020, estimates Roberts. SABIC (Riyadh, Saudi Arabia), he believes, will produce 5,000 metric tonnes (>11 million lb) by that same date, in Saudi Arabia and Italy, through its partnership with Montefibre SpA (Milan, Italy). He also called out Turkish manufacturer AKSA (Istanbul, Turkey), which recently formalized a joint venture with The Dow Chemical Co.’s (Midland, Mich.) European entity on Dec. 20, 2011, to commercialize carbon fiber products worldwide. Also new is a Toray Industries (Tokyo, Japan) line in South Korea; a Moses Lake, Wash., facility opened by SGL Automotive Carbon Fibers (Wiesbaden, Germany); Alabuga Fiber LLC (Tartarstan, Russia), which produces 1,500 metric tonnes (>3.3 million lb); and, he believes, an Iranian plant of unknown capacity. According to Roberts, “Every country wants a carbon fiber plant,” and more announcements will come from South Korea and South America before year’s end.

Roberts also reported that 18 companies in China claim to produce polyacrylonitrile (PAN) with a combined nameplate (maximum) capacity of 9,200 tonnes (nearly 20.3 million lb). Plants range, in theory, from 30 to 1,500 metric tonnes (66,140 to 3.3 million lb). Yet sources inside China say actual production is between 500 and 1,000 metric tonnes (1.1 million and 2.2 million lb). To address the glaring discrepancy, Roberts compared the reported 2010 market demand for carbon in China (9,785 metric tonnes/21.572 million lb) against reported imports of carbon fiber into that country (8,737 metric tonnes/19.262 million lb). The comparison of imports to demand shows that internal production is not yet meaningful. “The Chinese are currently working on improving the quality and performance of their fiber,” he stated.

Red is less enthusiastic than some about the adoption of carbon composites in cars: “It will be another decade before we see massive adoption of composites in automotive.” Representatives from Oak Ridge National Laboratory (ORNL, Oak Ridge, Tenn.) were more optimistic, in a preconference seminar on low-cost carbon fiber for the automotive market. ORNL is actively involved in several partnerships, including one with Dow, to explore the market for automotive carbon fiber made from alternative precursors, including lignin, olefin and polyethylene. And recent announcements of partnerships between carmakers and carbon producers portend an upsurge in automotive composites: General Motors (Detroit, Mich.) recently teamed with Teijin Ltd. (Tokyo, Japan) to push a part-per-minute process for carbon-fiber car parts, and a BMW and SGL Technologies GmbH (Wiesbaden, Germany) joint venture is already producing carbon fiber for two of BMW’s forthcoming battery-powered BMW electric commuter cars (see “SGL Automotive ….” under “Editor’s Picks,” at top right).

Red forecasts that aerospace demand (Table 3) will increase by 180 percent during the next decade, with 95 percent of that fiber delivered as unidirectional or woven prepregs. For industrial components (Table 4), he predicts 310 percent growth, with energy applications dominating the space. Consumer applications (Table 5), a more mature market, will grow a mere 47 percent in the next 10 years. By 2020, says Red, industrial uses will dwarf all others, with wind energy, by far, the largest in that space.

Is there enough precursor?

The final presenter, Service, painted a less rosy picture of the coming decade. After he explained the fiber production process, including the various precursor solvent technologies employed, he reiterated Roberts’ and Red’s predictions that carbon fiber sales will increase to 80,000 or 90,000 metric tonnes (176.4 million to 198.4 million lb) by 2015, with major growth in the industrial sector. But he warned that because 2.2 lb of precursor is required to make 1 lb of carbon fiber, nearly 300,000 metric tonnes (661.4 million lb) would be required in 2015, almost double the output of 2011. Although global acrylonitrile production per year is 6 million metric tonnes (13.227 billion lb), the chemical is a necessary feedstock for many products. Further, its cost is steep, currently between $1,500 and $3,000 per metric tonne, which directly affects precursor cost. He estimates that it will take about $30 million to build a plant capable of 1,000 metric tonnes (2.2 million lb) of PAN precursor annually, and he’s unaware of any near-term plans for big new facilities or plant expansions. Given these precursor, realities, Service estimates that the per-pound cost is now $10.90, up 32 percent compared to 2001.

So … on to maturity, or a return to cyclical downturns for lack of capacity? That question has been asked every year for decades, Roberts points out. Greater use of carbon fiber now appears inevitable. How that demand will be met is unclear, but emerging fiber producers, fiber recycling efforts and fibers from alternative precursors might yet and forever smooth the ups and downs of the industry.

If you liked this article, please give it a quick review on ycombinator or StumbleUpon. Thanks

Brian Wang is a Futurist Thought Leader and a popular Science blogger with 1 million readers per month. His blog Nextbigfuture.com is ranked #1 Science News Blog. It covers many disruptive technology and trends including Space, Robotics, Artificial Intelligence, Medicine, Anti-aging Biotechnology, and Nanotechnology.

Known for identifying cutting edge technologies, he is currently a Co-Founder of a startup and fundraiser for high potential early-stage companies. He is the Head of Research for Allocations for deep technology investments and an Angel Investor at Space Angels.

A frequent speaker at corporations, he has been a TEDx speaker, a Singularity University speaker and guest at numerous interviews for radio and podcasts. He is open to public speaking and advising engagements.