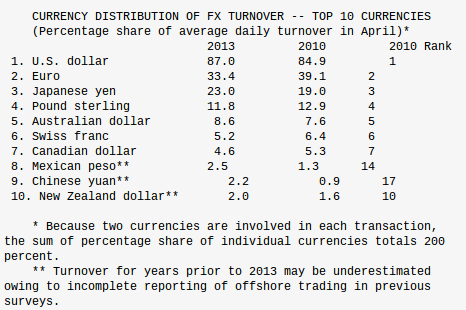

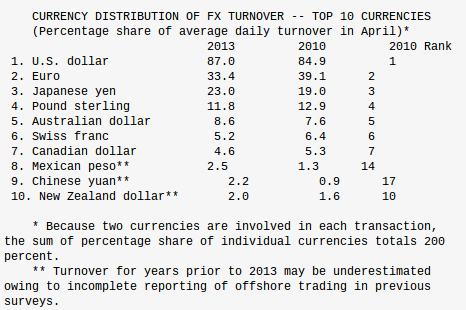

A triennial report on global foreign exchange activity from the Bank of International Settlements showed Thursday that trading in the yuan had tripled since the BIS’s 2010 survey, when it placed 17th in the world. In contrast, the BIS estimates showed that total global foreign exchange trading grew by 33% to $5.3 trillion over the three-year period.

While the government has quietly opened up a number of avenues for foreigners to participate in its capital markets, the capital flows into and out of the yuan are miniscule compared with other currencies. That should change: the government’s stated intent is to achieve “full convertibility” within the current five-year plan ending in 2015, though Beijing’s definition of that might fall short of the liberal trading regimes prevailing for the dollar, euro and British pound.

What translated this trade dominance into foreign exchange growth over the past three years, however, was the creation of centers for trading offshore versions of the yuan, first in Hong Kong, then in cities such as Singapore, London and New York. That allowed myriad businesses that trade with Chinese exporters and importers to hedge their exposures through spot and forward currency transactions.

Meanwhile, steps are being taken to open flows through the capital account, with one Chinese central bank official arguing Thursday that the time is right for more liberalization.

The Chinese currency will be fully convertible within five years, while a third of China’s trade will be settled in yuan by 2015, HSBC Holdings Plc forecast in a March report. This would mean at least another tripling of RMB currency activity by 2015. However, there is a stickiness problem that will prevent rapid switching to a new currency after another currency has been chosen for a project.

Here is a summary of the Bank of International Settlements report

Tripling China RMB usage by 2015 would put the RMB as about the 6th most used currency. China seems likely to get to 4th most used by 2018-2020 even with a conservative plan of capital liberalization.

China should want to get more RMB usage because it offers to make their economy more efficient and would force more efficiency on their banks. It offers increased economic growth. For the rest of the world it would mean even more outflows of capital from chineses individuals and companies able to buy and invest more overseas. This has already had a large impact on real estate in Canada, California, Australia and some Asian countries.

The big bang will come when portfolio flows are liberalized in the domestic market and when it becomes easier for holders of offshore yuan to transfer them into mainland bank accounts.

Various projects are underway in this regard, though their scale is small. Certain “qualified” foreign institutional investors can now invest in Chinese stocks and Treasury bond listed on domestic exchanges. And in July, state news agency Xinhua reported that the quota for this program would be raised to $150 billion from $80 billion while participation would be expanded beyond institutions in Hong Kong to include Singapore and London.

Separately, the region of Qianhai in Shenzhen is being earmarked for a trial expansion in cross-border lending between Hong Kong and the mainland.

An argument about China’s currency is that China’s failure to move from partial convertibility of the yuan (confined to conversion for current trade in goods and services) to full convertibility (including international capital transactions) is responsible for misallocation of China’s own capital resources as well as the inability of China’s policymakers, no less than of their critics, to estimate the yuan’s “true” exchange value.

Their model suggests that the share of the RMB in export invoicing should have been higher than the actual share of less than 10%. The underperformance of the RMB export invoicing can be attributed to the inertia of the choice of currency for trade invoicing; once a currency is used for trade invoicing or settlements, it becomes difficult for traders to switch from one currency to another. That was also observed in the cases with the Japanese Yen and the Euro in their inceptions as international currencies. Their model predicts the share of RMB invoicing for China’s exports would rise up to above 25% in 2015 and above 30% in 2018 whether or not China implements drastic financial liberalization. Because the RMB is also expected to experience the inertia in the near future, these predictions will probably be the upper end of the actual path of RMB export invoicing.

In contrast, in the dimension of use as a store of value, the rise of the RMB or “redback” is a potential challenge to the current international monetary system that is heavily dependent on the U.S. dollar only in the longer term. While the United States accounts for 20% of global output, 11% of trade, and 30% of financial asset trade, about 60% of foreign exchange reserves are held in U.S. dollars in the world.

Many argue that such a dollar-centric international monetary system creates an unstable environment for the world economy by providing the U.S. with privileged access to funds (“exorbitant privilege”), while constraining developing economies with the opposite effect (i.e., “original sin,” the inability to issue sovereign debt in own currency). As Eichengreen (2011) argues, a new international monetary with multiple reserve currencies — the U.S. dollar, the Euro,

and the Chinese Yuan — might be more stable than the current unipolar system. That is because the loss of exorbitant privilege by the US would discipline the nation’s public finance.

The conventional wisdom holds that the arrival of that multipolar international currency system is a long way off, although there are dissenters. With the RMB the only viable competitor amongst emerging market economies (Chinn, 2012), the issue of internationalization of the Chinese Yuan is now a global issue. Nonetheless, because most observers believe that major reserve currency status for the Yuan is a long way off, we will focus on the private actor roles of an international reserve currency – the use in trade invoicing and in denomination of assets.

Whether and how fast the RMB becomes an international currency depends on some key points. First, how soon and in what ways China implements two policies: allowing greater market determination of the value of the Yuan, and liberalizing transactions of capital across its borders. The value of the currency needs to be able to fluctuate freely, so that international investors can read signals from the market and consider portfolio strategy accordingly. Investors need to be able to find it easy to acquire or redeem Yuan-denominated bonds at their convenience in terms of both time and location. Both these conditions appear far off.

If you liked this article, please give it a quick review on ycombinator or StumbleUpon. Thanks

Brian Wang is a Futurist Thought Leader and a popular Science blogger with 1 million readers per month. His blog Nextbigfuture.com is ranked #1 Science News Blog. It covers many disruptive technology and trends including Space, Robotics, Artificial Intelligence, Medicine, Anti-aging Biotechnology, and Nanotechnology.

Known for identifying cutting edge technologies, he is currently a Co-Founder of a startup and fundraiser for high potential early-stage companies. He is the Head of Research for Allocations for deep technology investments and an Angel Investor at Space Angels.

A frequent speaker at corporations, he has been a TEDx speaker, a Singularity University speaker and guest at numerous interviews for radio and podcasts. He is open to public speaking and advising engagements.