HSBC has a report “The World Economy’s Titanic Problem” which indicates that in the event of a future recession, the world economy has run out of traditional stimulus. HSBC Chief Economist Stephen King says the US Federal Reserve has had to cut rates by over 500 basis points to right the ship in each of the recessions since the early 1970s.

Budget deficits are still uncomfortably large and debt levels uncomfortably high: while the US fiscal position has improved, it remains structurally weak.

We investigate the options for policymakers given this shortage of traditional ammunition, including:

(i) reducing the risk of recession;

(ii) reverting to quantitative easing;

(iii) moving away from inflation targeting;

(iv) using fiscal policy to replace monetary policy;

(v) using fiscal and monetary policy together in a bid to introduce so-called “helicopter money”; and

(vi) pushing interest rates higher through structural reforms designed to lower excess savings, most obviously via increases in retirement age.

We conclude that only the final option is likely to lead to economic success. Politically, however, it seems implausible. As a result, we are faced with a serious shortage of effective policy lifeboats.

As for plausible recession triggers, we highlight four major risks:

1) a rise in US wages which leads to a falling profit share and a major equity decline

2) a series of systemic failures within the non-bank financial sector

3) a major weakening of the Chinese economy, sending shockwaves around the world; and

4) a premature attempt by the Federal Reserve to normalise monetary policy, in a repeat of the mistakes made by the Bank of Japan in 2000 and, more recently, by the European Central Bank in 2011.

Recovery but not recovered to Normal

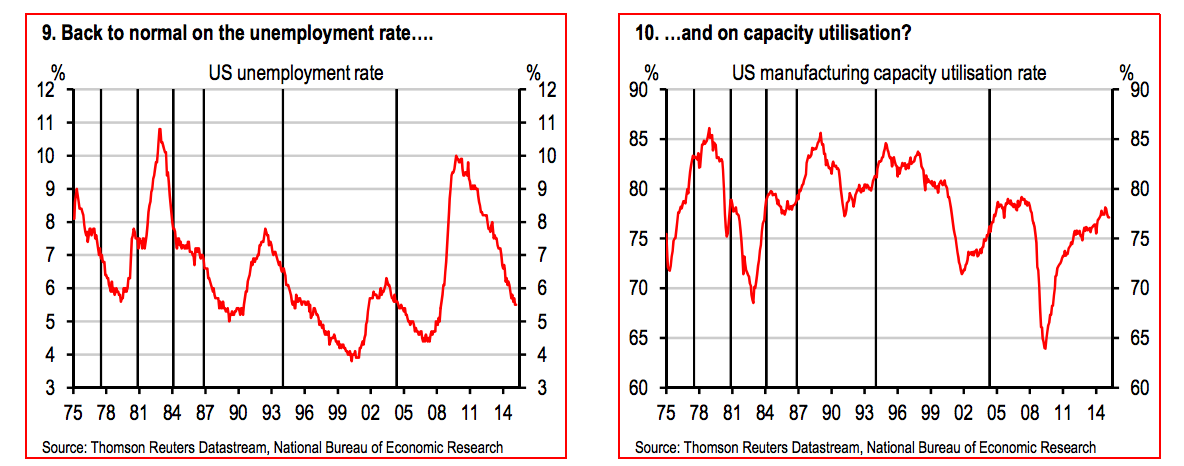

In most economic cycles, the recovery phase has not just marked a return to economic growth. It has also, eventually, marked a return to policy “normality”. Interest rates have risen. Tax revenues have rebounded. Welfare payments have shrunk. Budget deficits have declined – and, on some occasions, have even turned into surpluses. Put another way, a return to economic growth typically allows policymakers to rebuild their stocks of ammunition, providing them with room to fight the next economic battle.

This latest economic cycle is, to date, fundamentally different. According to the National Bureau of Economic Research, the last trough in US economic activity was reached in June 2009. Almost six years into recovery, official short-term interest rates haven’t budged an inch. 10 year Treasury yields are at rock bottom, still lower than they were in the immediate aftermath of the collapse of Lehman Brothers in 2008. The Federal budget deficit has dramatically improved but the fiscal position is nothing like as healthy as it typically has been through previous economic cycles.

One reason for this lack of action – this failure to rebuild stocks of ammunition – is simply that the pace of economic recovery has not been particularly strong. The latest recovery is particularly weak. Then again, so was the previous recovery. Back then, however, the Federal Reserve was able to raise interest rates 31 months after the trough in economic activity. This time, 70 months have elapsed (at the time of writing) and still the Fed hasn’t acted.

Brian Wang is a Futurist Thought Leader and a popular Science blogger with 1 million readers per month. His blog Nextbigfuture.com is ranked #1 Science News Blog. It covers many disruptive technology and trends including Space, Robotics, Artificial Intelligence, Medicine, Anti-aging Biotechnology, and Nanotechnology.

Known for identifying cutting edge technologies, he is currently a Co-Founder of a startup and fundraiser for high potential early-stage companies. He is the Head of Research for Allocations for deep technology investments and an Angel Investor at Space Angels.

A frequent speaker at corporations, he has been a TEDx speaker, a Singularity University speaker and guest at numerous interviews for radio and podcasts. He is open to public speaking and advising engagements.