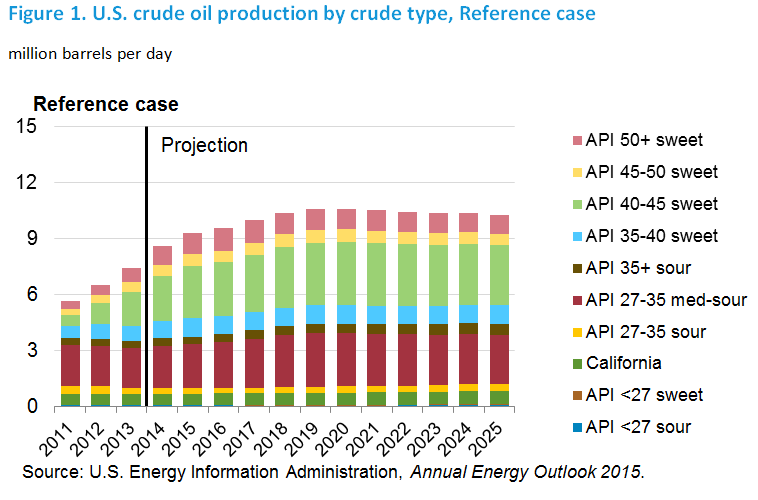

When US crude oil production gets past 10.1 million barrels per day then it will have passed the old production peak in 1970.

This will take a further increase of about 500,000 barrels per day. About 5% more production.

Getting to 11 million barrels per day is the the low oil price case.

The High Oil and Gas Resource case in AEO2015 was developed using assumptions that result in higher estimates of technically recoverable crude oil and natural gas resources than those in the Reference case. Estimates of technically recoverable tight and shale crude oil and natural gas resources are particularly uncertain and change over time as new information is gained through drilling, production, and technology experimentation. The assumptions for the High Oil and Gas Resource case are very optimistic.

Specific assumptions for the High Oil and Gas Resource case, as compared with the Reference Case, include:

• 50% higher estimated ultimate recovery (EUR) levels for tight oil, tight gas, and shale gas wells

• Additional tight oil resources, as well as 50% lower well spacing per acre (i.e., wells are closer together), with a downward limit of 40 acres per well for existing and potential future tight oil resources, to capture the possibility that additional layers or new areas of low-permeability zones will be identified and developed

• Diminishing returns on the EUR when drilling in a county exceeds the number of potential wells assumed in the Reference case, to capture the probability that greater drilling density will cause wells to interfere with each other (i.e., production from one well might reduce production from a nearby well)

• Long-term technology improvements beyond those assumed in the Reference case, represented as a 1% annual increase in the EURs for tight oil, tight gas, and shale gas wells

• 50% higher technically recoverable undiscovered resources for Alaska crude oil and the Lower 48 offshore, reflecting the uncertainty surrounding undeveloped areas where there has been little or no exploration and development activity, and where modern seismic survey data are lacking

The High Oil and Gas Resource case does not include exploration or production activity in the Arctic National Wildlife Refuge or other areas that are currently under drilling moratoria.

In the High Oil Price case, crude oil prices quickly rise to $149/bbl (Brent, 2013 dollars) in 2020 and $169/bbl in 2025 compared with $79/bbl and $91/bbl in the Reference case, respectively.

In the Low Oil Price case, the Brent crude oil price drops to $52/bbl in 2015, 7% lower than in the Reference case, and reaches $64/bbl in 2025, 30% lower than in the Reference case, largely as a result of lower non-OECD demand and higher upstream investment by OPEC

Gulf of Mexico Production is still heading up

Because of the long timelines associated with Gulf of Mexico (GOM) projects, the recent downturn in oil prices is expected to have minimal direct impact on GOM crude oil production through 2016. EIA projects GOM production to reach 1.52 million barrels per day (bbl/d) in 2015 and 1.61 million bbl/d in 2016, or about 16% and 17% of total U.S. crude oil production in those two years, respectively.

The forecasted production growth is driven both by new projects and the redevelopment and expansion of older producing fields. Five deepwater projects began in the last three months of 2014: Stone Energy-operated Cardamom Deep and Cardona projects, Chevron-operated Jack/St. Malo fields, Murphy Oil-operated Dalmatian, and Hess-operated Tubular Bells. Also occurring at the end of 2014 was the redevelopment of Mars (Mars B) and Na Kika (Na Kika Phase 3), both of which are mature fields. Cardamom Deep, Jack/St. Malo, and Tubular Bells were slated for a late 2014 start-up, as well.

Developments are forecast to boost Gulf production by 265,000 barrels per day by the end of 2015.

What about Peak oil and the peak oil theorists ?

Gail makes the case that peak oil is manifesting as a Glut of oil and a glut of all other commodities. She worries about high debt and affordability. She indicates that is a networked economy which causes the “unusual effects”.

One way of viewing our problem today is as a crisis of affordability. Young people cannot afford to start families or buy new homes because of a combination of the high cost of higher education (leading to debt), the high cost of fuel-efficient new cars (again leading to debt), the high cost of resale homes, and the relatively low wages paid to young workers.

Meanwhile, the Peak Oil diehards like Ron Patterson claims that global peak oil will happen in 2015 and US crude oil production will again stop rising in 2015.

Brian Wang is a Futurist Thought Leader and a popular Science blogger with 1 million readers per month. His blog Nextbigfuture.com is ranked #1 Science News Blog. It covers many disruptive technology and trends including Space, Robotics, Artificial Intelligence, Medicine, Anti-aging Biotechnology, and Nanotechnology.

Known for identifying cutting edge technologies, he is currently a Co-Founder of a startup and fundraiser for high potential early-stage companies. He is the Head of Research for Allocations for deep technology investments and an Angel Investor at Space Angels.

A frequent speaker at corporations, he has been a TEDx speaker, a Singularity University speaker and guest at numerous interviews for radio and podcasts. He is open to public speaking and advising engagements.