China’s economy has grown enormously over the past three-and-a-half decades. Its gross domestic product (GDP), the most common measure of economic output, was $10.4 trillion in 2014, making it the world’s second-largest economy—only the U.S. economy is larger.2 This growth has propelled China’s standard of living, formerly one of the lowest in the world, to a level that the World Bank characterizes as “upper middle income.” China’s annual per capita GDP rose from $1,300 in 1980 to $7,700 in 2010, an increase of almost 500 percent.

Using fundamental growth theory, data from China and from Korea and Japan’s similar “miracle” growth experiences, we provide a suggestive calculation for China’s future per capita income. Our ballpark estimate is that China’s per capita income relative to that of the United States will grow by a factor of two to three over the next half-century.

Calculation implies that China will improve its per capita income at a faster pace than that of the United States for about the next 45 years. By around 2061, it will reach close to half of the U.S. income per capita. While China’s income per capita relative to the United States will more than double from today, its absolute income per capita will increase by much more, by about a multiple of five.

On a PPP per capita GDP basis, the IMF has current year estimates of per capital GDP and future year forecasts 2016 $15095 [About 26% of US per capita level, 85th in the world] 2017 $16172 2018 $17405 2019 $18752 2020 $20190 2021 $21733 [about 32% of US level, 79th in the world] Overall China economy would 132% of the US economy on PPP basis

There are other papers that look at China’s per capita GDP convergence.

China’s Economic Growth and Convergence by Jong-Wha Lee (51 pages)

Economic Growth and Convergence, Applied Especially to China”, by Robert Barro

Robert Barro looked at countries that had at least doubled real per capita GDP since 1990. Within this group, he defined a middle-income success as having achieved a level of real per capita GDP in 2014 of at least $10,000. An upper-income success requires a level of at least $20,000 (the numbers are in 2011 US dollars and factor in international adjustments for changes in purchasing power).

With these criteria, the world’s middle-income convergence success stories comprise China, Costa Rica, Indonesia, Peru, Thailand, and Uruguay (Uruguay is a surprise, apparently boosted by dramatic migration of human capital out of Argentina.) The upper-income successes consist of Chile, Hong Kong, Ireland, Malaysia, Poland, Singapore, South Korea, and Taiwan.

A view that has gained recent popularity is the ‘middle-income trap’. According to this idea, the successful transition from low- to middle-income status is typically followed by barriers that impede a further transition to upper income. The data suggest that this trap is a myth. Moving from low- to middle-income status, as achieved recently by China, is difficult. Conditional on achieving middle-income status, the further transition to upper-income status is also difficult. However, there is no evidence that this second transition is harder than the first one.

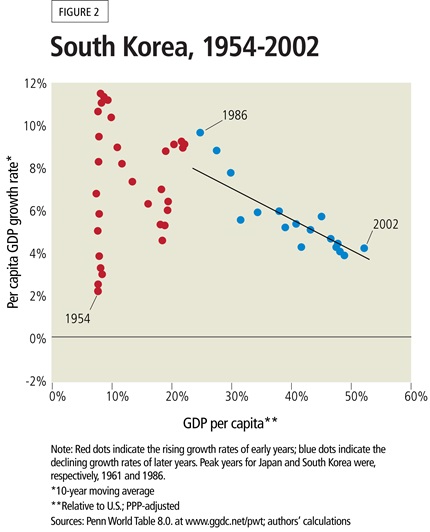

SOURCES – Minneapolis Fed, South Korea research, VoxEU

Brian Wang is a Futurist Thought Leader and a popular Science blogger with 1 million readers per month. His blog Nextbigfuture.com is ranked #1 Science News Blog. It covers many disruptive technology and trends including Space, Robotics, Artificial Intelligence, Medicine, Anti-aging Biotechnology, and Nanotechnology.

Known for identifying cutting edge technologies, he is currently a Co-Founder of a startup and fundraiser for high potential early-stage companies. He is the Head of Research for Allocations for deep technology investments and an Angel Investor at Space Angels.

A frequent speaker at corporations, he has been a TEDx speaker, a Singularity University speaker and guest at numerous interviews for radio and podcasts. He is open to public speaking and advising engagements.