The standard theoretical framework for development economics was established more than 50 years ago by the MIT economist Robert Solow, who developed a mathematical model that predicts countries’ economic growth on the basis of labor and capital (the tools of production); subsequent work expanded the model to include factors such as land and human capital (expert knowledge). The model proved highly influential, ultimately earning Solow the 1987 Nobel Prize in economics.

Hidalgo argues, by lumping together a huge variety of resources under the general heading “capital,” it can obscure distinctions that are crucial to an accurate understanding of countries’ economies. In a series of papers cowritten with Ricardo Hausmann, director of the Center for International Development at Harvard’s Kennedy School of Government, Hidalgo has argued that, indeed, the best predictor of a country’s future economic health is not the magnitude but the diversity of its production capacity.

Economists think of production in terms of inputs and outputs. The outputs are the goods that a country produces. The inputs are everything that’s required to produce those goods. In 19th-century America, lumber was an example of a product with relatively few inputs. Exporting it required little more than the manpower and tools to chop down trees and haul them to shipping ports. Twentieth-century digital-signal-processing chips, on the other hand, are products that require a lot of inputs: the ability to extract and purify exotic materials like gallium arsenide, computer-aided design software to produce circuit layouts, and the chemicals and vacuum chambers required for the deposition of different layers of material, among other things.

Hidalgo and Hausmann argue that the diversity of a country’s production capacity, and thus the true strength of its economy, depends on the diversity of both its outputs and its inputs. Two countries could export the same number of products — they could have the same diversity of outputs — but if one exports only garments, it’s likely to have many fewer inputs than a country that exports a mix of garments and other light manufacturing, agricultural products, electronics and cultural goods. And the country with more inputs, the researchers claim, will adapt better to a changing world economy.

It’s an intuitively plausible claim, but getting a quantitative handle on it is difficult. Diversity of outputs is easy enough to measure: Economists have developed some standard schemes for classifying products that have borne up well in empirical studies. But almost anything could count as an input: not just natural resources or factories but, say, a good public-transportation system that makes the labor market more efficient, or intellectual-property laws that reward entrepreneurship.

That’s where Hidalgo’s mathematical tools come in. Rather than try to exhaustively categorize inputs — probably an impossible task — Hidalgo simply assumes that products that require a lot of inputs are scarcer than those that don’t: More countries export lumber than export digital-signal-processing chips. By analyzing both the diversity of a country’s products and the number of other countries capable of producing the same products, Hidalgo is able to quantitatively assess the diversity of the country’s inputs.

Cash value

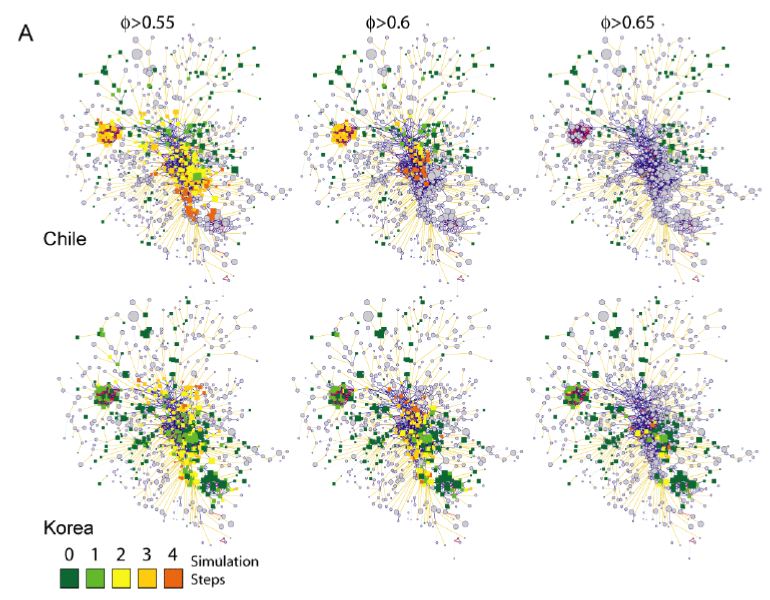

Hidalgo and Hausmann have found that GDP correlates pretty well with diversity of outputs, but it correlates much better with diversity of inputs. And the cases where the correlation breaks down could actually be more interesting than the cases where it holds, because they could indicate economies poised for growth. In 1970, for instance, the Korean economy had much greater diversity of inputs, according to Hidalgo’s measure, than the Peruvian economy; but Peru had twice Korea’s GDP per capita. Over the next 30 years, the relative diversity of inputs in the two countries’ economies stayed more or less the same, but by 2003, Korea had four times Peru’s GDP per capita.

Moreover, Hidalgo points out, Korea’s surge is impossible to explain using the standard factors of production. “In 1970, Peruvian workers were working with four times the capital per worker, and they were working with two and a half times the land per worker, and they had the same level of education as Korean workers,” Hidalgo says.

Arxiv – The Product Space Conditions the Development of Nations

E

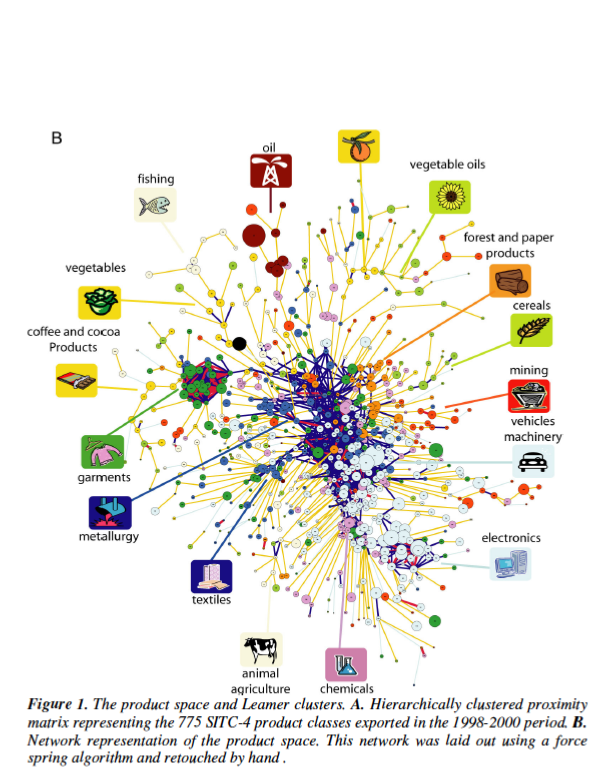

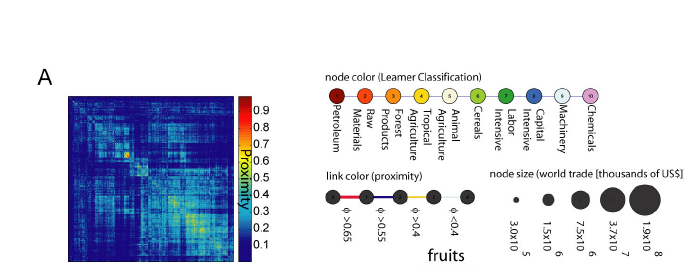

conomies grow by upgrading the type of products they produce and export. The technology, capital, institutions and skills needed to make such new products are more easily adapted from some products than others. We study the network of relatedness between products, or product space, finding that most upscale products are located in a densely connected core while lower income products occupy a less connected periphery. We show that countries tend to move to goods close to those they are currently specialized in, allowing nations located in more connected parts of the product space to upgrade their exports basket more quickly. Most countries can reach the core only if they jump over empirically infrequent distances in the product space. This may help explain why poor countries have trouble developing more competitive exports, failing to converge to the income levels of rich countries.

In this paper we have mapped the product space, and studied how countries dynamically

evolve on it. We empirically proved that countries develop RCA following a diffusion

process for which our outcome based definition of the product space appears to be the

natural substrate. Moreover, the structure of the product space limits the diffusion process by being non-traversable by jumps of any proximity. When we combine these results with the fact that poorer countries tend to have RCA mainly on peripheral products, it implies that a country’s productive structure is constrained not only by its levels of factor endowments, but also by how easily those product-specific factors can be adapted to alternative uses, as indicated by location in the product space. On a more global perspective, these results point towards a new hypothesis for the lack of income convergence in the world: convergence can only exist if countries have the ability to reach any area of the product space. Our study shows that most of the diffusion occurs through links with proximities of 0.6 or larger, thus the most popular strategy involves diffusing to nearby products, a strategy that is successful for richer countries located on the core of the space, and ineffective for poorer countries populating the periphery.

If you liked this article, please give it a quick review on ycombinator or StumbleUpon. Thanks

Brian Wang is a Futurist Thought Leader and a popular Science blogger with 1 million readers per month. His blog Nextbigfuture.com is ranked #1 Science News Blog. It covers many disruptive technology and trends including Space, Robotics, Artificial Intelligence, Medicine, Anti-aging Biotechnology, and Nanotechnology.

Known for identifying cutting edge technologies, he is currently a Co-Founder of a startup and fundraiser for high potential early-stage companies. He is the Head of Research for Allocations for deep technology investments and an Angel Investor at Space Angels.

A frequent speaker at corporations, he has been a TEDx speaker, a Singularity University speaker and guest at numerous interviews for radio and podcasts. He is open to public speaking and advising engagements.