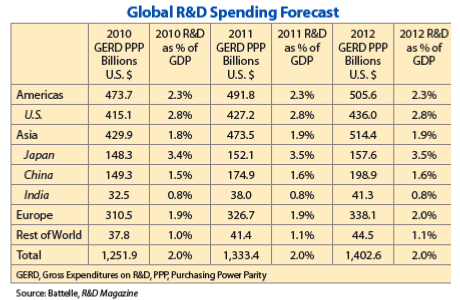

The Battelle-R and D Magazine annual Global R and D Funding Forecast released today shows global research and development (R and D) spending is expected to grow by about 5.2 percent in 2012 to more than $1.4 trillion. R and D funding growth will largely be driven by Asian economies—a number projected to increase by nearly 9 percent in 2012. Elsewhere in the world, growth remains strong and stable in the aftermath of the global recession.

Batelle 2012 Global R and D Funding Forecast (36 pages)

European R&D will grow by about 3.5 percent while North American R&D will grow by 2.8 percent.

Experts from Battelle and R and D Magazine forecast that a 2.1 percent growth in United States R and D expenditures will be balanced against an estimated 2 percent inflation rate, suggesting that U.S. R and D investments will remain flat in real terms over the next year. That $436 billion in forecasted spending is expected to be broken down in the following way:

* U.S. Private Industry will spend by far the largest amount with a projection of $279.6 billion in R&D in 2012, up 3.75 percent over 2011.

* U.S. Federal Government spending will reach $125.6 billion in 2012, a decrease of 1.16 percent.

* Academia in the U.S. will spend $12 billion on research in 2012, up 2.85 percent over last year.

* Non-profits will increase spending in 2012 by 2.7 percent to $14.5 billion and other government entities in the U.S. will round out total R and D expenditures by increasing 2.72 percent to $3.8 billion.Aerospace and Defense: U.S. federally funded defense R and D will reach nearly $75 billion in 2012, exceeding every other country’s total R and D except that of China, Japan and Germany. The increasing importance of and reliance on unmanned and autonomous vehicles and real-time situational awareness and sensor systems continue to change the aerospace, defense and national security R&D landscape. Beyond this level of federally funded R and D, U.S. corporations also will invest $13.8 billion of their own resources on R and D activities in 2012, up 5.9 percent from 2011. Globally, aerospace and defense industry R and D spending will grow by 1.9 percent to reach $26.2 billion in 2012.

These systems, by their nature and scale, provide system-level R and D opportunities that historically were limited to major prime contractors with large manufacturing capacities. These larger companies likely will dominate the R and D expenditures, but many smaller companies are also engaged both as subcontractors and primes in significant efforts in these technological areas.

Early-stage and D efforts in these technologies, along with efforts in other sensor and monitoring technologies, cybersecurity, nanotechnology and advanced materials, biofuels and medical technologies will see continued defense R and D funding, for which numerous smaller firms may see a more level playing field during the next five to 10 years.

Energy: Energy-related research sponsored by U.S. manufacturers and technology providers will reach nearly $6.7 billion in 2012, up 23.1 percent from 2011. Global spending by energy-related companies will grow by 7.8 percent to reach $17.9 billion in 2012.

A review panel commissioned by the U.S. Department of Energy (DOE) identified key R&D areas where DOE program and investment can play a significant development role, including several in which the DOE historically has underinvested. The areas address both energy supply and demand and relate to both stationary power (deploying clean electricity, modernizing the grid and increasing building/industrial efficiency) and transport power (deploying alternative hydrocarbon fuels, electrifying the vehicle fleet, and increasing vehicle efficiency).

The panel calls on DOE to maintain a mix of analytic, assessment and fundamental engineering research capabilities in a broad set of energy-technology areas while seeking to balance more assured activities against higher-risk transformational work. At the same time, the report acknowledges that the efforts must be relevant to the private sector. There is a tension between supporting work that industry doesn’t—the long term nature of basic research—and the urgency of the nation’s energy challenge.

Life Science: United States R&D spending in the life science industry is expected to decline by 5.7 percent to $73.2 billion in 2012 as pharmaceutical firms tighten their R&D budgets. Global R&D spending in the industry also is forecast to decline by 2.2 percent to $147.3 billion.

This sector includes such diverse firms as multi-national pharmaceutical corporations, large medical device and instrument companies and both large and small biotechnology firms.

A major change in the funding and performing of life science R&D is the convergence in public and private sector R&D toward open innovation and open source information—especially in areas needing considerable fundamental research. It is due, in part, to the pharmaceutical industry’s retrenchment from its conventional model to a more reduced internal R&D function and focuses more on collaboration and ROI. The ripple effects of impending patent expirations and the widely reported decline in productivity in the development and approval of significant new medicines are driving the strategic changes.

Information and Communication Technologies (ICT): During the past two years, ICT-related manufacturing has been particularly volatile, with leading companies experiencing commercial dynamics following the introduction of new products arising from R&D decisions. Despite these fluctuations the United States’ R&D spending in the ICT industry is forecast to increase by 9.9 percent, reaching $138.8 billion in 2012. This U.S. growth helps drive an overall global ICT industry growth of 4.1 percent to $238.5 billion.

The Funding Forecast highlights several high profile companies as examples of how success in the ICT marketplace cannot be maintained simply by being the current market leader and making large R&D investments. A clear vision of long-term technology goals aligned with a competitive marketing strategy is essential.

Information from The Economist’s Intelligence Unit (EIU) affirms that the U.S. remains the world’s most competitive country in ICT, but notes that developing nations are beginning to close the gap. The U.S. and Japan make up nearly 70 percent of all global ICT investments.

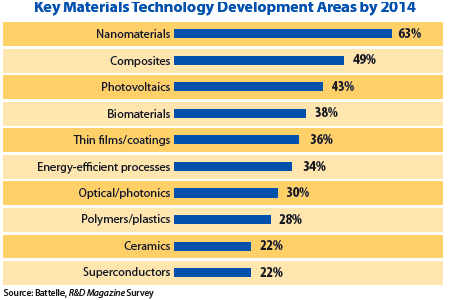

Chemicals and Materials: R&D in the broadly defined chemicals and materials industry is expected to grow by 11.4 percent in the U.S. to $9.3 billion in 2012, while growing by 3.8 percent globally to $33.8 billion.

Nanotechnology and its applications continue to pervade all industrial applications with biomedical applications beginning during the past two years. More than 15 U.S. government agencies propose funding $2.13 billion in nanotechnology research including DOE at $611 million, the National Institutes of Health at $465 million, the National Science Foundation at $456 million and the Department of Defense at $368 million.

An emerging priority in advanced materials is a heightened focus on developing alternative sources or processes related to rare earth metals because of China’s recent export limits on supplies. In the industrial sector around the world, closed non-Chinese rare earth mines are being re-opened; however, the environmental requirements for operating these mines have increased since they closed, making additional R&D and capital expenditures necessary to develop new and improved processing programs.

If you liked this article, please give it a quick review on ycombinator or StumbleUpon. Thanks

Brian Wang is a Futurist Thought Leader and a popular Science blogger with 1 million readers per month. His blog Nextbigfuture.com is ranked #1 Science News Blog. It covers many disruptive technology and trends including Space, Robotics, Artificial Intelligence, Medicine, Anti-aging Biotechnology, and Nanotechnology.

Known for identifying cutting edge technologies, he is currently a Co-Founder of a startup and fundraiser for high potential early-stage companies. He is the Head of Research for Allocations for deep technology investments and an Angel Investor at Space Angels.

A frequent speaker at corporations, he has been a TEDx speaker, a Singularity University speaker and guest at numerous interviews for radio and podcasts. He is open to public speaking and advising engagements.