The Economist magazine examines the question – Is the age of the growth miracle at an end?

Harvard economist Dani Rodrik, in which he argued that the age of the “growth miracle” was over. Industrialisation, long the engine of economic development, is becoming less able to support catch-up growth, he suggested, thanks to the falling labour-intensity of manufacturing, Chinese competition, and a rising mercantilist tide across the rich world.

Richard Baldwin, whose research on a supply-chain-oriented view of globalisation and development was recently featured in the print edition, strongly disagrees:

The truth is that globalization has been driven by advances in two very different types of “connective” technologies: transportation and transmission. Up till the late 1980s, globalization was mostly about lower trade and transportation costs. This “first unbundling” of production was associated with rising G7 shares of world income and trade…

Since then, globalization has mostly been about lower communications and transmission costs. This “second unbundling” of production has seen G7 shares of world income and trade fall dramatically. Globalization’s second unbundling involves two phenomena:

* Fractionalisation (unbundling of supply chains into finer stages of production); and

* Geographic dispersion of the unbundled stages.Global supply chains (GSCs) are the connective tissue that allows fractionalized and dispersed stages to operate as a harmonious whole.

GSCs transformed the world by allowing poor nations to join supply chains rather than investing decades in building up their own. This is where Rodrik’s analysis falls down. He calls these “growth miracles” because he overlooks the fundamental change in the nature of globalization that enabled them

Before the 1980s – Catching the leaders meant building an entire supply chain from the ground up—and in the teeth of competition. Development was slow, laborious and rare. Japan and South Korea grew industries from modest beginnings. They entered global markets with inferior but cheap products, often supported by state aid, then slowly improved their technical competence. Painstaking accumulation of technological skill eventually enabled innovative multinational firms to emerge. Japanese and South Korean incomes converged with those in western Europe. Other emerging economies tried gamely to duplicate this success, to little avail. Aggressive industrial policies often strained government resources without delivering a critical mass in industry or the human capital needed for development.

A new model began to emerge in the 1980s. Lower transport costs were a catalyst. Yet more important, reckons Mr Baldwin, was a budding revolution in information and communication technology (ICT). Cheaper communications allowed firms to manage supply chains over ever greater distances. Companies discovered they could build plants in cheap locations, ship components there to be assembled and export the finished product around the world. While the first unbundling separated producing markets from consuming markets, the second broke up production entirely across long, multinational supply chains.

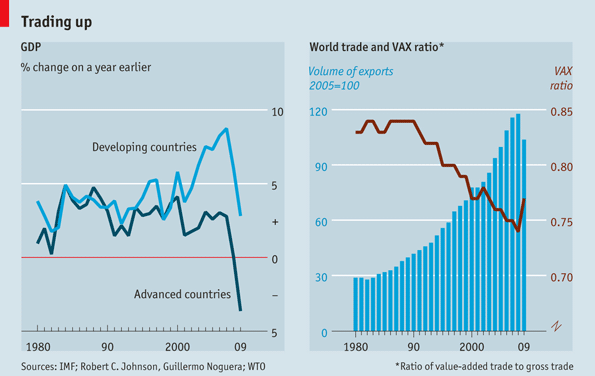

That made industrialisation a cakewalk compared with earlier times. A business-friendly government and cheap workers were often sufficient to get started; foreign firms provided technology and management. Emerging markets quickly signed on. Trade data analysed by Robert Johnson of Dartmouth College and Guillermo Noguera of Columbia University track the shift. Along multinational supply chains, they note, a single component may be exported several times, adding to tallies of gross trade but not to measures of value added. A fall in the ratio of the two measures (which they call the VAX) signifies an increase in supply-chain fragmentation. On this score, 1990 seems a critical point, after which the VAX sinks while trade volumes soar (see chart above). Emerging-market growth surged at roughly that time.

Faster growth may be fickle growth, says Mr Baldwin. Whereas previous tigers built a deep technological capacity, many emerging markets now merely “borrow” technology from rich-world firms. Multinationals have an incentive to limit technology transfer, the better to preserve the bargaining power that comes with a credible threat to leave. Learning can still occur. China uses its size as leverage to extract concessions, often confining direct inward investment to joint ventures between foreign and domestic firms, for instance. Smaller markets lack that option. The limited spillovers from supply-chain industrialisation may leave them stuck in middle-income status. And there is always the risk that chains may shift again, leaving them high and dry.

When Korea, the US and Germany were doing it, building an industrial base took decades due to learning-by-doing with complex complementaries; roughly speaking, manufacturers had to get almost every right before anything was right.

The rise of global supply chains now means that advanced-technology firms arrive with everything but the labour—technical know-how, managerial capacity, quality control, logistic and organisation infrastructure; they even bring the customers (themselves). Thus everything works from the start; industrialisation zooms ahead. Rodrik—thinking that globalisation is still working the way it did when Korea and Taiwan were developing—has to call it a miracle because it doesn’t fit into the 19th and 20th century trade and development paradigms he learned as a student and renovated as a researcher.

In short, China’s growth was not due the rich-nation policymakers “looking the other way”. It was due to rich-nation firms teaching low-wage workers and managers how to produce world class parts and components, or how to assemble them into world-competitive final goods. As wages in China rise, Chinese firms are now giving similar lessons to Bangladeshi and Vietnamese workers and firms.

A key intellectual blinder in all this—one that Rodrik suffers from in much of his writing—is the notion that technology is country-specific. Before the information and communication technology revolution this might have been a good approximation, but now that it is easier to control the application of know-how abroad, we have discovered that technology is primarily firm-specific.

As Baldwin argues in his recent paper for the Fung Global Institute, the future of global supply chains—and thus the path of new economic miracles—will be influenced by four key determinants:

1. Improvements in coordination technology that lower the cost of functional and geographical unbundling,

2. Improvements in computer integrated manufacturing that lower the benefits of specialisation and shift stages toward greater skill-, capital-, and technology-intensity,

3. Narrowing of wage gaps that reduces the benefit of North-South offshoring to nations like China, and

4. The price of oil which raises the cost of unbundling.Two key messages emerge from the analysis. First convergent wages and income level between “factory economies” and “headquarter economies” need not reduce supply-chain trade. The intensity of such trade among developed nations exceeds that between developed and emerging nations since the gains from specialisation driven by firm-level excellence is even more important than the gains from specialisation due to large wage gaps. A foundational tenant of trade theory is that nations trade more—not less—as their economies get larger and more similar. Second, narrowing wage gaps between China and developed nations are likely to produce a continuation of the old “flying geese” pattern whereby early developers move up the value chain and thereby encourage the next low-wage nation to step on to the development ladder.

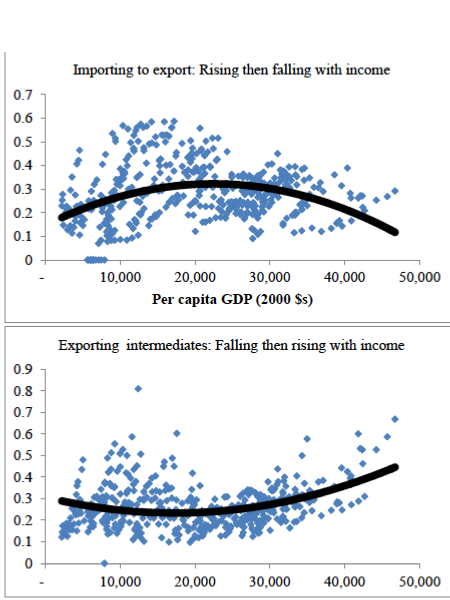

There are some clear empirical regularities linking a nation’s level of development – as measure by per capita income – and its backwards and forwards supply-chain trade.

* As nations get richer up to a point, they use imported intermediates more intensively in their exports. Beyond a threshold – about $25,000 per year per person – the intensity diminishes (top panel below).

* For forward supply-chain trade – i.e. the supply of intermediates to others – the relationship is flipped. It falls for low income levels but rises beyond a point near $15,000 (second panel).

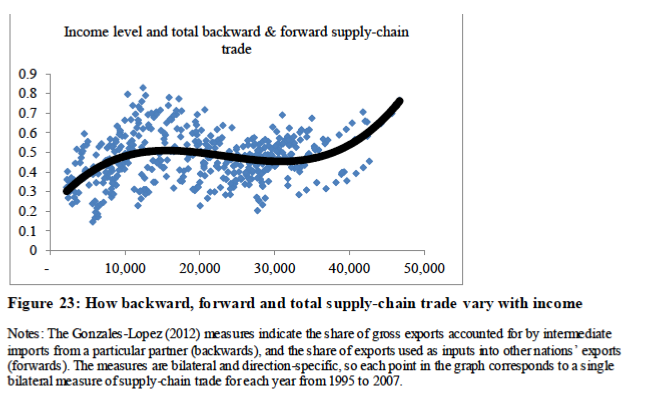

Combining the two measures, we get a nation’s total involvement in supply-chain (see panel below).

If you liked this article, please give it a quick review on ycombinator or StumbleUpon. Thanks

Brian Wang is a Futurist Thought Leader and a popular Science blogger with 1 million readers per month. His blog Nextbigfuture.com is ranked #1 Science News Blog. It covers many disruptive technology and trends including Space, Robotics, Artificial Intelligence, Medicine, Anti-aging Biotechnology, and Nanotechnology.

Known for identifying cutting edge technologies, he is currently a Co-Founder of a startup and fundraiser for high potential early-stage companies. He is the Head of Research for Allocations for deep technology investments and an Angel Investor at Space Angels.

A frequent speaker at corporations, he has been a TEDx speaker, a Singularity University speaker and guest at numerous interviews for radio and podcasts. He is open to public speaking and advising engagements.