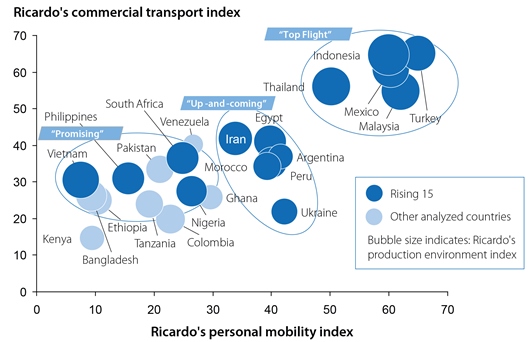

From 2020 onwards the study predicts that the engine for profitable growth will be – political stability provided – the economies of Ricardo’s ‘Rising-15’ automotive markets: Argentina, Egypt, Indonesia, Iran, Malaysia, Mexico, Morocco, Nigeria, Peru, the Philippines, South Africa, Thailand, Turkey, Ukraine, and Vietnam.

Taken together, Ricardo’s ‘Rising-15‘ – which has a combined population of 1.2 billion – is already the third largest vehicle market in the world, with annual sales exceeding 8.5 million vehicles in 2012. These sales are equivalent to the combined total of the four largest European vehicle markets – Germany, UK, France and Italy. Average annual growth across the ‘Rising-15’ has exceeded 9% for the past 10 years – and in most of these countries, Ricardo found, vehicle markets have grown faster than the economy as a whole.

“The impending maturity and repeated hiccups in growth of the BRIC economies in the latter part of the current decade have been predicted by many industry observers,” commented Ricardo Strategic Consulting managing director for Central Europe, Andreas Schlosser. “There have been winners and losers in the efforts of the current cohort of established global automakers to exploit growth within the BRIC region; the key strategic question now is where the next wave of growth based opportunity will arise. By analysing the world’s fast-growing economies in some detail, we have been able to highlight what we are calling the ‘Rising-15’ markets which will present the key opportunity to 2025 and beyond. The insights provided by this work will be of interest to the established global automotive brands as well as to the emerging global automakers of the BRIC region with strategic aspirations to move beyond their domestic markets and compete at an international level.”

Triad markets move beyond their peak, while the BRICs stumble

The study indicates that the traditional triad markets of Europe, North America and Japan and Korea will continue to stagnate, with automakers struggling to reach pre-2008 vehicle sales levels. While demand falters, however, not all sectors are being affected equally, with lifestyle, premium and budget vehicles performing significantly more strongly than the squeezed mid-market sector brands previously favoured by middle-class purchasers. With signs of overcapacity already becoming apparent within the triad and the BRIC regions alike, stronger localization policies will combine with increasing competition to make these markets less attractive to global automakers.

By the end of the current decade, it concludes that the more liberal markets and rapidly developing economies of the ‘Rising-15’ will offer significant new opportunities for the global automotive industry. With vehicle ownership strongly correlated to GDP per capita, the study indicates that the fast growing ‘Rising-15’ markets still offer the biggest potentials for automotive growth. In markets such as these, a further qualitative trend in vehicle purchase has been the substitution of imported used vehicles with budget vehicle brands. But as with previous waves of international automotive expansion, competition in this new phase of growth will be joined by new players – particularly from China and India – with aspirations for global expansion. The long-term insights provided by the full study are likely to be extremely valuable to the entire automotive value chain in all parts of the world.

If you liked this article, please give it a quick review on ycombinator or StumbleUpon. Thanks

Brian Wang is a Futurist Thought Leader and a popular Science blogger with 1 million readers per month. His blog Nextbigfuture.com is ranked #1 Science News Blog. It covers many disruptive technology and trends including Space, Robotics, Artificial Intelligence, Medicine, Anti-aging Biotechnology, and Nanotechnology.

Known for identifying cutting edge technologies, he is currently a Co-Founder of a startup and fundraiser for high potential early-stage companies. He is the Head of Research for Allocations for deep technology investments and an Angel Investor at Space Angels.

A frequent speaker at corporations, he has been a TEDx speaker, a Singularity University speaker and guest at numerous interviews for radio and podcasts. He is open to public speaking and advising engagements.