The Annual Energy Outlook 2015 (AEO2015), prepared by the U.S. Energy Information Administration (EIA), presents long-term annual projections of energy supply, demand, and prices through 2040. The projections, focused on U.S. energy markets, are based on results from EIA’s National Energy Modeling System (NEMS). NEMS enables EIA to make projections under alternative, internally-consistent sets of assumptions, the results of which are presented as cases. The analysis in AEO2015 focuses on six cases: Reference case, Low and High Economic Growth cases, Low and High Oil Price cases, and High Oil and Gas Resource case.

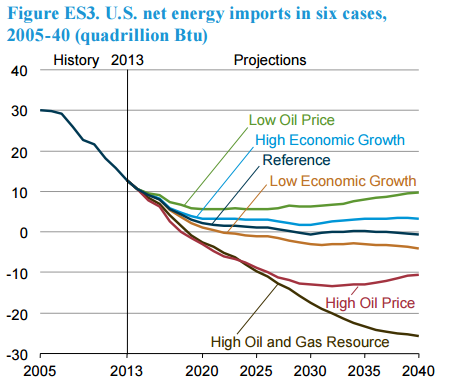

• Through 2020, strong growth in domestic crude oil production from tight formations leads to a decline in net petroleum imports and growth in net petroleum product exports in all AEO2015 cases. In the High Oil and Gas Resource case, increased crude production before 2020 results in increased processed condensate exports. Slowing growth in domestic production after 2020 is offset by increased vehicle fuel economy standards that limit growth in domestic demand. The net import share of crude oil and petroleum products supplied falls from 33% of total supply in 2013 to 17% of total supply in 2040 in the Reference case. The United States becomes a net exporter of petroleum and other liquids after 2020 in the High Oil Price and High Oil and Gas Resource cases because of greater U.S. crude oil production.

• The United States transitions from being a modest net importer of natural gas to a net exporter by 2017. U.S. export growth continues after 2017, with net exports in 2040 ranging from 3.0 trillion cubic feet (Tcf) in the Low Oil Price case to 13.1 Tcf in the High Oil and Gas Resource case.

• Rising costs for electric power generation, transmission, and distribution, coupled with relatively slow growth of electricity demand, produce an 18% increase in the average retail price of electricity over the period from 2013 to 2040 in the AEO2015 Reference case. The AEO2015 cases do not include the proposed Clean Power Plan

Brent crude oil price reflects the world market price for light sweet crude, and all the cases account for market conditions in 2014, including the 10% decline in the average Brent spot price to $97/barrel (bbl) in 2013 dollars.

In the AEO2015 Reference case, continued growth in U.S. crude oil production contributes to a 43% decrease in the Brent crude oil price, to $56/bbl in 2015 (Figure ES1). Prices rise steadily after 2015 in response to growth in demand from countries outside the OECD; however, downward price pressure from continued increases in U.S. crude oil production keeps the Brent price below $80/bbl through 2020. U.S. crude oil production starts to decline after 2020, but increased production from non-OECD countries and from countries in the Organization of the Petroleum Exporting Countries (OPEC) contributes to the Brent price remaining below $100/bbl through 2028 and limits the Brent price increase through 2040, when it reaches $141/bbl.

There is significant price variation in the alternative cases using different assumptions. In the Low Oil Price case, the Brent price drops to $52/bbl in 2015, 7% lower than in the Reference case, and reaches $76/bbl in 2040, 47% lower than in the Reference case, largely as a result of lower non-OECD demand and higher upstream investment by OPEC. In the High Oil Price case, the Brent price increases to $122/bbl in 2015 and to $252/bbl in 2040, largely in response to significantly lower OPEC production and higher non-OECD demand. In the High Oil and Gas Resource case, assumptions about overseas demand and supply decisions do not vary from those in the Reference case, but U.S. crude oil production growth is significantly greater, resulting in lower U.S. net imports of crude oil, and causing the Brent spot price to average $129/bbl in 2040, which is 8% lower than in the Reference case.

SOURCES – EIA

Brian Wang is a Futurist Thought Leader and a popular Science blogger with 1 million readers per month. His blog Nextbigfuture.com is ranked #1 Science News Blog. It covers many disruptive technology and trends including Space, Robotics, Artificial Intelligence, Medicine, Anti-aging Biotechnology, and Nanotechnology.

Known for identifying cutting edge technologies, he is currently a Co-Founder of a startup and fundraiser for high potential early-stage companies. He is the Head of Research for Allocations for deep technology investments and an Angel Investor at Space Angels.

A frequent speaker at corporations, he has been a TEDx speaker, a Singularity University speaker and guest at numerous interviews for radio and podcasts. He is open to public speaking and advising engagements.