Russia has fallen into full-blown depression and faces a mounting fiscal crisis as oil and gas revenues plummet. Output from country’s state-owned gas giant Gazprom has collapsed by 19pc over the past year as demand shrivels in Europe.

The Russian authorities have the crisis under control for now. They have allowed the ruble to fall rather than burning up reserves, providing a cushion for the budget and for oil and gas producers. But this policy is inflationary, and politically toxic.

It is 66 rubles to 1 US dollar

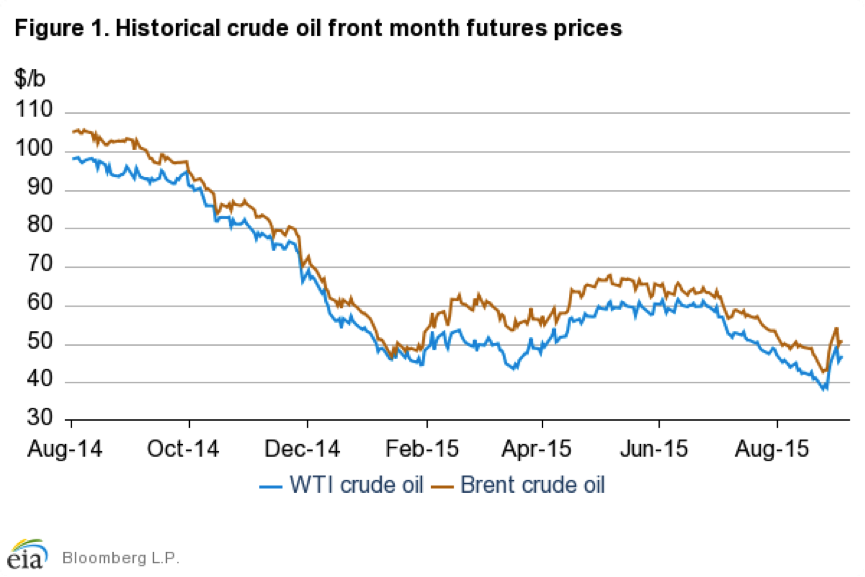

In March 2015, the government was forced to amend the budget in order to adapt to the $50 oil price level, and it is likely that the 2016 budget will also be tailored accordingly.

Russia has been able to weather the challenges facing its economy a bit better than Nextbigfuture thought they would back in March 2015. However, if oil prices stay low it seems to be a matter of time (1 to 4 years) before Russia has a bigger crisis. With China’s economy in what appears to be long term slower growth, it seems oil prices could stay at $60 per barrel or less through 2020.

Gazprom’s revenues are likely to drop by almost a third to $106bn this year from $146bn in 2014, seriously eroding Russia’s economic base. Gazprom alone generates a tenth of Russian GDP and a fifth of all budget revenues.

The economy has contracted by 4.9pc over the past year and the downturn is certain to drag on as oil prices crumble after a tentative rally. Half of Russia’s tax income comes from oil and gas.

“Russia is going to be in a very difficult fiscal situation by 2017,” said Lubomir Mitov from Unicredit. “By the end of next year there won’t be any money left in the oil reserve fund and there is a humongous deficit in the pension fund. They are running a budget deficit of 3.7pc of GDP but without developed capital markets Russia can’t really afford to run a deficit at all.”

The official reserves have dropped from $524bn to $361bn since the Ukraine crisis first erupted in late 2014. Unicredit said the true figure is nearer $340bn once other commitments are stripped out.

New Investment and Foreign Technology needed to maintain Oil Production by 2018

They are still relying on old Soviet wells,” said Mr Mitov. The depletion rates in the traditional fields of Western Siberia are running at 8pc-11pc a year.

“They can’t keep up production without access to foreign imports and technology, so we think there could be a fall in output of 5pc to 10pc by 2018,” he said.

Lukoil’s vice-president, Leonid Fedun, said in March that Russia’s oil output could fall 8pc by the end of next year, taking 800,000 barrels a day (b/d) out of global markets, with major implications for the balance of supply and demand.

Any such loss would be corrosive for Russia. It has not happened yet. Russian producers have taken advantage of a new tax regime to raise output this year to 10.7m b/d, close to the post-Soviet peak. But they are relying on legacy investments and imported machinery that must be replaced sooner or later.

Putin’s long-term strategy depends on opening up the Arctic and the vast shale reserves of the Bazhenov basin and the Volga-Urals. Drilling in these regions is covered by sanctions, forcing Western firms to freeze joint ventures.

Russia lacks the technology to make these projects viable. Average fracking costs in Russia are three times higher than those of cutting-edge drillers in the US.

SOURCES – Telegraph UK, Bloomberg, Global Risk Insights

Brian Wang is a Futurist Thought Leader and a popular Science blogger with 1 million readers per month. His blog Nextbigfuture.com is ranked #1 Science News Blog. It covers many disruptive technology and trends including Space, Robotics, Artificial Intelligence, Medicine, Anti-aging Biotechnology, and Nanotechnology.

Known for identifying cutting edge technologies, he is currently a Co-Founder of a startup and fundraiser for high potential early-stage companies. He is the Head of Research for Allocations for deep technology investments and an Angel Investor at Space Angels.

A frequent speaker at corporations, he has been a TEDx speaker, a Singularity University speaker and guest at numerous interviews for radio and podcasts. He is open to public speaking and advising engagements.