The richest 1% now has as much wealth as the rest of the world combined, according to Oxfam.

The Oxfam press release is based upon Credit Suisse wealth report which the James Davies, Rodrigo Lluberas , and Anthony F. Shorrocks global wealth distribution analysis.

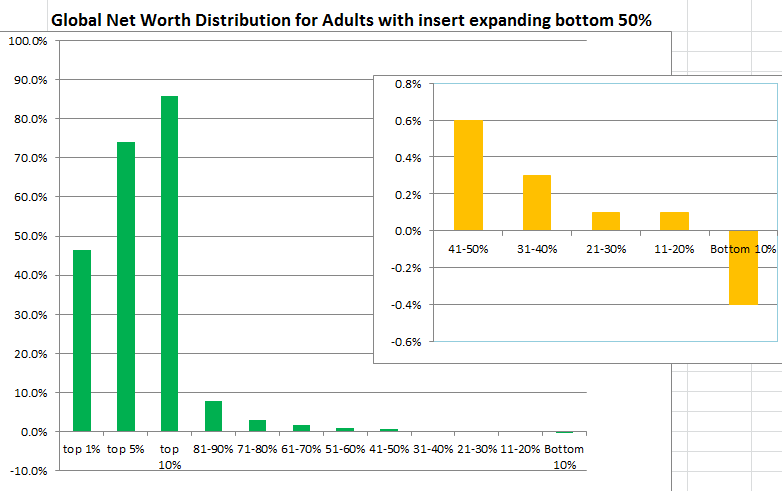

The bottom 10% have a collective negative $1.05 trillion net worth (-0.4% of $263 trillion). Each of the poorest 720 million people have an average of -$1450 in net worth per individual in the bottom 10%.

The poorest owe more than they own.

It takes three people who are almost as poor to make up for that debt.

Poorest in bottom 10% -$1450 Poor but in 11-20% +$250 Poor but in 21-30% +$350 Poor but in 31-37% +$850

wealth = real assets + financial assets – debts

Negative net worth causes interesting statistics

Oxfam can say the 62 richest people having as much wealth as the poorest 50% of the population is a remarkable concentration of wealth. But the poorest person in the world has more net worth than the bottom 37%. This is because the bottom 10% are in debt and are debt. The more of the most in debt people you add up then the more negative it gets until you get to people who own a little more than they owe.

More on the poorest

The income of the poorest had very little change from 2011 data.

The wealth data changed from 2011 for the bottom 10% where the estimate went from -0.4% of $263 trillion in overall world wealth from -0.2% of 240 trillion. The top billionaires increased wealth by 8% each year from 2011.

Chart based upon 2013 wealth distribution data from Davies, Lluberas and Shorrocks

A 10% move from the 2013 wealth distribution puts the top 1% with 50% of world wealth. They went from 45% of the wealth to a little over 50%.

The 2015 Credit Suisse October report on wealth distribution (158 pages has details).

The net worth of the middle class in 2015 amounted to USD 80.7 trillion worldwide, or 32% of global wealth. Adults with wealth beyond the middle class threshold accounted for a further USD 150 trillion, bringing the total wealth of the middle class and beyond to USD 231 trillion, or 92% of global wealth. Thus the 1 in 6 adults who belong to the middle class and beyond own the vast bulk of global assets.

For each country the upper limit of middle class wealth is ten times the lower bound. This allows the members of the middle class to be identified, and their number and wealth to be estimated. Credit Suisse results indicate that 664 million adults belong to the global middle class in 2015, equivalent to 14% of the total adult population. A further 96 million (2% of world adults) have wealth above the upper bound of our middle class wealth range.

For a variety of reasons including the iconic status of the middle class in North America the United States is chosen as the benchmark country. Specifically, a middle class adult in the United States is defined to be one with wealth between USD 50,000 and USD 500,000 valued at mid-2015 prices. The lower bound could perhaps be justified by noting that USD 50,000 equates to roughly two years median earnings, and hence provides substantial protection against work interruptions, income shortfalls, or emergency expenditures. Similarly, the upper threshold of USD 500,000 roughly equates to the amount of capital a person close to retirement age needs to purchase an annuity paying the median wage for the remainder of their life. However, we do not aim to provide a detailed justification of our chosen cut-offs, which are intended to be indicative rather than precise. Other reasonable values for the lower and upper bounds do not appear to change the broad patterns and conclusions documented below.

For the years before 2015, the middle class wealth bounds for the United States were adjusted downwards using the US CPI. For other countries, the IMF series of purchasing power parity (PPP) values was used to derive middle class wealth bounds equivalent in local purchasing power terms. Nowadays prices in the United States are often lower than in other advanced economies, so applying the PPP adjustment sometimes produces lower bounds for middle class wealth above USD 50,000. Among Nordic countries, for example, the cut-offs in 2015 range from USD 51,400 for Finland and USD 52,600 for Sweden to USD 57,300 for Denmark and USD 58,200 for Norway. Applying our methodology suggests that an adult in Switzerland must own at least USD 72,900 in assets to belong to the middle class.

Countries with lower wealth per capita tend to have lower prices, so for them the middle class threshold is correspondingly reduced, as Table 1 shows. To be a member of the middle class in 2015 according to our methodology, an adult needs at least USD 28,000 in Brazil, Chile and China; USD 22,000 in South Africa and Turkey; USD 18,000 in Malaysia, Russia and Thailand; and just USD 13,700 in India.

One of the most important is that data constraints prevent Credit Suisse from applying different wealth bounds to different age groups. Credit Suisse bounds are likely to be less appropriate for the young than the middle aged, and they may also be questionable for the very old. This lays Credit Suisse open to the suggestion that the exclusion of young people with wealth less than USD 50,000 is the reason why just 38% of adults qualify as middle class in the United States. However, Credit Suisse believe this criticism carries little weight. Australia and the United States have similar demography, for example. Yet 66% of adults in Australia qualify as middle class on our methodology. This suggests that high wealth inequality is the principal reason for the low middle class numbers found here for the United States rather than the exclusion of too many young or old people.

Some commentators recommend including the value of state pensions in the definition of wealth, which would lead to a rise in the size of the middle class, especially in high income countries. However, we do not favor this option. People have legal ownership of their private pensions. In contrast, social security wealth can be changed by government policy. Large private pensions give people a source of security and independence that makes them solidly middle class. Those who depend on the state for their retirement income are not in the same category

To construct the global distribution of wealth, the level of wealth derived for each country was combined with details of its wealth pattern. Specifically, the ungrouping program was applied to each country to generate a set of synthetic sample values and sample weights consistent with the (estimated or imputed) wealth distribution. Each synthetic sample observation represents 10,000 adults in the bottom 90% of the distribution, 1,000 adults in the top decile, and 100 adults in the top percentile. The wealth sample values were then scaled up to match the mean

wealth of the respective country.

Brian Wang is a Futurist Thought Leader and a popular Science blogger with 1 million readers per month. His blog Nextbigfuture.com is ranked #1 Science News Blog. It covers many disruptive technology and trends including Space, Robotics, Artificial Intelligence, Medicine, Anti-aging Biotechnology, and Nanotechnology.

Known for identifying cutting edge technologies, he is currently a Co-Founder of a startup and fundraiser for high potential early-stage companies. He is the Head of Research for Allocations for deep technology investments and an Angel Investor at Space Angels.

A frequent speaker at corporations, he has been a TEDx speaker, a Singularity University speaker and guest at numerous interviews for radio and podcasts. He is open to public speaking and advising engagements.