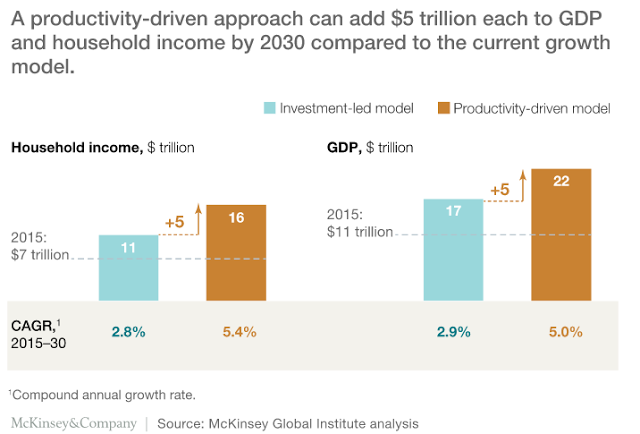

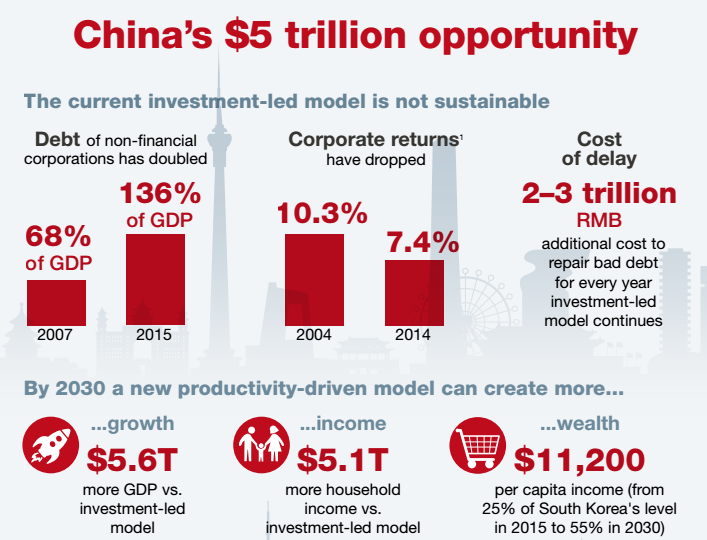

China faces an important choice: whether to continue with its old model and raise the risk of a hard landing for the economy, or to shift gears. A new McKinsey Global Institute report, China’s choice: Capturing the $5 trillion productivity opportunity, finds that a new approach centered on productivity could generate 36 trillion renminbi ($5.6 trillion) of additional GDP by 2030, compared with continuing the investment-led path. Household income could rise by 33 trillion renminbi ($5.1 trillion), as the exhibit shows.

China has the capacity to manage the decisive shift to a productivity-led model. Its government can pull fiscal and monetary levers, such as raising sovereign debt and securing additional financing on the basis of 123 trillion renminbi in state-owned assets. China has a vibrant private sector, earning three times the returns on assets of state-owned enterprises. There are now 116 million middle-class and affluent households (with annual disposable income of at least $21,000 per year), compared with just 2 million such households in 2000. And the country is ripe for a productivity revolution. Labor productivity is 15 to 30 percent of the average in countries that are part of the Organisation for Economic Co-operation and Development (OECD).

Making this transition is an urgent imperative. The longer China continues to accumulate debt to support near-term goals for GDP growth, the greater the risks of a hard landing. We estimate that the nonperforming-loan ratio in 2015 was already at about 7 percent, well above the reported 1.7 percent. If no visible progress is made to curb lending to poorly performing companies, and if the performance of Chinese companies overall continues to deteriorate, we estimate that the nonperforming-loan ratio could rise to 15 percent. This would trigger a substantial impairment of banks’ capital and require replenishing equity by as much as 8.2 trillion renminbi ($1.3 trillion) in 2019. In other words, every year of delay could raise the potential cost by more than 2 trillion renminbi ($310 billion). Although such an escalation would not lead to a systemic banking crisis, a liquidity crunch among corporate borrowers and waning confidence of investors and consumers during the recovery phase would have a significant negative impact on growth.

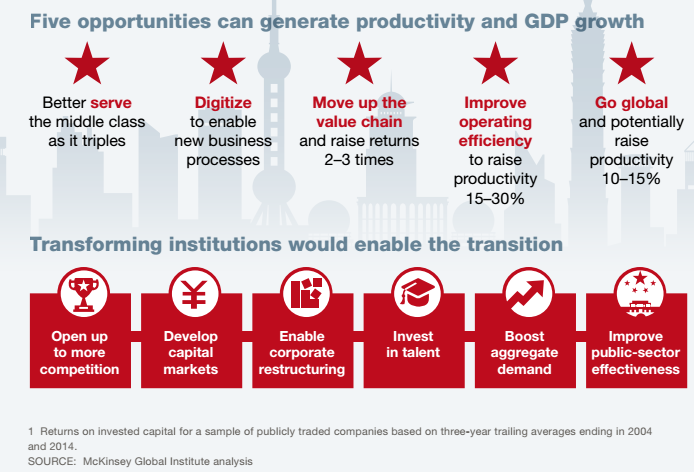

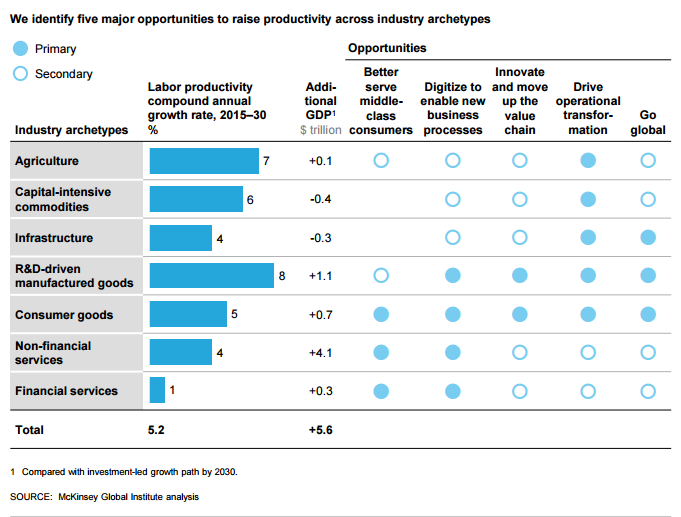

The report identifies five major opportunities to raise productivity by 2030:

- unleashing more than 39 trillion renminbi ($6 trillion) in consumption by serving middle-class consumers better

- enabling new business processes through digitization

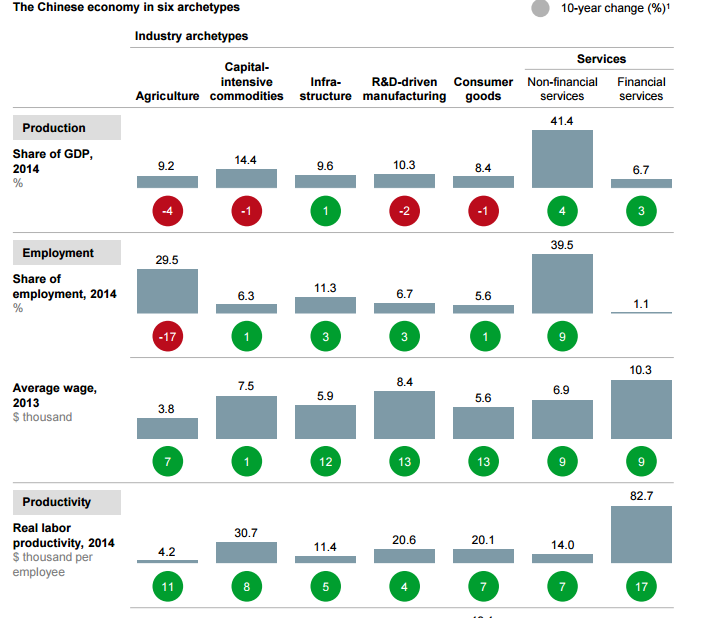

- moving up the value chain through innovation, especially in R&D-intensive sectors, where profits are only about one-third of those of global leaders

- improving business operations through lean techniques and higher energy efficiency, for instance, which could deliver a 15 to 30 percent productivity boost

- strengthening competitiveness by deepening global connections, potentially raising productivity by 10 to 15 percent

A CEO agenda for China’s potential new direction

McKinsey sees four ways that companies can navigate the transition.

- Take a bottom-up approach to understanding the market. Instead of focusing undue attention on short-term GDP growth rates, companies that want to make the most of the opportunities of China’s economy need to have a longer-term but also more detailed view. They need to identify what sectors are likely to thrive in a new productivity-led model. Markets in some cities and provinces will take off because highly productive industries are growing there; others will decline because the local economy has not performed well enough on productivity. Starbucks is one company that has opted to raise its long-term commitment to the Chinese market. The coffee chain now has 1,700 stores in more than 90 Chinese cities, and it plans to open 500 new stores per year to meet demand created by an expanding cohort of middle class consumers.

- Take bold measures to restructure businesses. When China was growing at 10 percent a year, companies in China were too busy keeping up with demand to devote sufficient attention and resources to making their operations internationally competitive. With growth slowing and the possibility of pressure on returns, companies need to take the opportunity to focus on raising productivity, judging which assets are genuinely strategic and how operations could be optimized. The sense of urgency that a more difficult business environment inspires can also be used to make a stronger push for innovation in products and business models, and to review resource allocation to support future growth.

- Be prepared for heightened global competition from China. Slower domestic growth may well force Chinese companies to seek new opportunities abroad, and companies everywhere should be prepared for heightened competition. Time spent getting to know these new competitors will be valuable in shaping opportunities to collaborate. For their part, Chinese companies will need to plot their international expansion strategically, choosing which markets to prioritize initially. Global ambitions among Chinese companies present an opportunity for new partnerships that, for instance, may fund next-generation technologies in autos or telecommunications.

- Enhance the speed and flexibility of decision making. The economic and political environment in China is likely to be dynamic over the coming decade; companies that cannot size up a fluid situation, decide what to do, and act with speed and agility could find themselves at a severe disadvantage. Companies need to streamline their decision making, constantly gathering information to inform their choices through frequent feedback from suppliers, customers, and partners. For foreign-based multinationals, there may not be time for proposals to travel through multiple layers of reporting to reach decision makers back at global headquarters. More local decision making and empowerment of local teams can help.

SOURCES- McKinsey

Brian Wang is a Futurist Thought Leader and a popular Science blogger with 1 million readers per month. His blog Nextbigfuture.com is ranked #1 Science News Blog. It covers many disruptive technology and trends including Space, Robotics, Artificial Intelligence, Medicine, Anti-aging Biotechnology, and Nanotechnology.

Known for identifying cutting edge technologies, he is currently a Co-Founder of a startup and fundraiser for high potential early-stage companies. He is the Head of Research for Allocations for deep technology investments and an Angel Investor at Space Angels.

A frequent speaker at corporations, he has been a TEDx speaker, a Singularity University speaker and guest at numerous interviews for radio and podcasts. He is open to public speaking and advising engagements.