Morgan Stanley and Michael Pettis differ on what China’s sustainable economic growth rate is over the next ten to fifteen years China. Morgan Stanley, however, proposes that China can manage to grow at an average annual rate above 5 percent for the next ten years, which suggests that they think this sustainable growth rate today is around 6 percent or a little less. Pettis thinks China is unlikely to manage growth rates above 3 percent on average, and probably much lower.

Key Metrics for China’s future economic growth

* China’s Debt to GDP is about 260% now – China can keep pushing GDP growth until debt to GDP is about 350% of GDP. Then it will be whatever the natural sustainable GDP growth rate level is

* The Sustainable growth rate for the next 10-15 years seems to be between 3 to 5%

* If China can get private consumption up from about $5 trillion now to $12-15 trillion in 2025 then China will be able to sustain a higher GDP growth rate level

Morgan Stanley thinks that by 2030, household disposable income will reach $8,700; the median age will rise to 43, and internet penetration will increase to 75%; compared to $5,000, 37 years old, and 52%, respectively, in 2016.

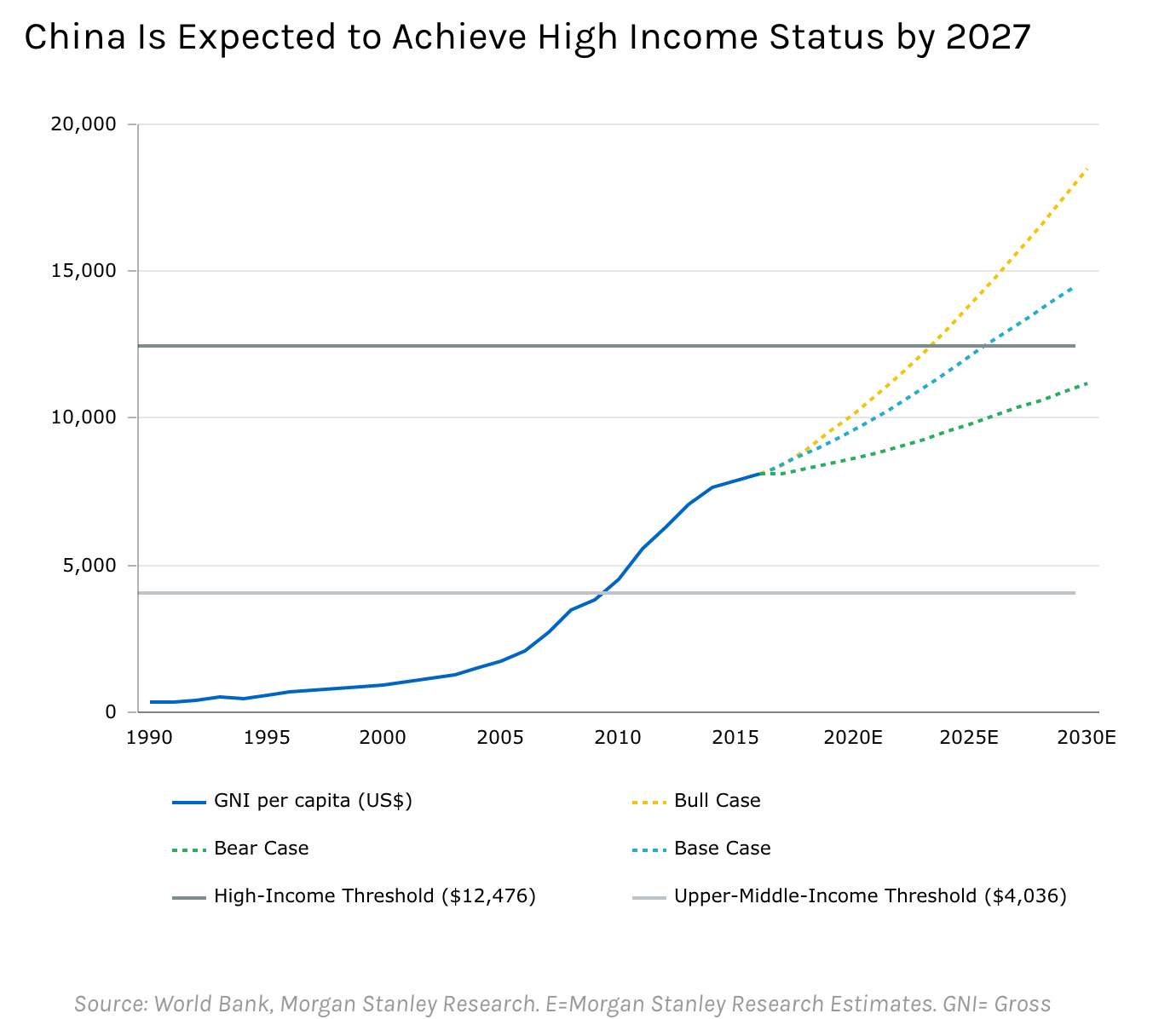

Morgan Stanley has a Bluepaper called “Why We Are Bullish on China.” The report makes the most cogent version of the bull case for China and predicts that average GDP growth rates over the next ten years will exceed 5 percent, turning China into a high-income country by 2027.

Morgan Stanley forecasts that “China will break out of the middle-income trap and join the rarified ranks of high-income society” attaining per capita GNI of above $12,500 by 2027.

China’s economy would then be about US$17.5 trillion on a nominal GDP basis in current dollars. China would then be close to the level of the US economy. The actual level relative to the USA would depend on the currency exchange rate.

Chetan Ahya, Morgan Stanley’s Co-Head of Global Economics and Chief Asia Economist. Of particular concern: China’s debt has risen from 147% of GDP in 2007 to 279% in 2016, a buildup that many fear is unsustainable. Reflecting their skepticism, investors now hold a decade-low underweight position in China equities, notes Jonathan Garner, Morgan Stanley’s Chief Asia Equity Strategist.

Still, China has proven its mettle in the past. In the aftermath of both global financial crises—in 1998 and 2008—even as many market stalwarts faltered, China held fast as an anchor of economic stability.

Ahya and Garner believe that it can avoid the worst yet again, citing three major factors:

* China’s own savings have funded its buildup in debt, which has gone into investment, rather than consumption;

* The government enjoys strong net asset positions both domestically and externally. Both provide adequate buffers against shocks;

* Strong external macro positions, including a current account surplus, high levels of foreign currency reserves, and lack of significant inflationary pressures, leave China with plenty of leeway to manage domestic liquidity conditions.

That said, “China has borrowed a lot from the future, and the payback will be in the form of a significant slowdown in growth rates,” Ahya says.

Pettis also thought that China would average 3% GDP growth from 2010 to 2020. China’s growth has been higher.

GDP growth above a sustainable rate requires an acceleration in credit growth. This is the only way to generate the additional demand needed to boost economic activity to a level, the GDP growth target, that is politically acceptable. So how much debt is needed to generate how much additional growth above the sustainable growth rate?

China needs to keep debt below 350-400% of GDP

March’s 2.1 trillion renminbi increase in debt was part of a 7.0 trillion renminbi increase in debt in the first quarter of 2017, an amount equal to an astonishing 39 percent of the country’s first quarter GDP. Part of this increased lending was used simply to roll over bad debt that is not being recognized. But most of it went to fund a 13.6 percent increase in public sector investment.

Pettis thinks the increase in debt was needed to add the 3–4 percentage points. He assumes this is the minimum gap between China’s sustainable growth rate and its actual growth rate. Morgan Stanley—and anyone else who believes that China can manage a decade or more of 5 percent growth is saying the large debt boosts growth by only one percentage point above the rate China can achieve anyway without relying on debt.

Another possible explanation consistent with Morgan Stanley’s numbers. They might assume that the vast bulk of credit creation over the past few years has occurred purely as speculative froth, has not generated any demand in the Chinese economy, and so can be eliminated overnight without impacting growth at all.

Private Consumption

Brian Wang is a Futurist Thought Leader and a popular Science blogger with 1 million readers per month. His blog Nextbigfuture.com is ranked #1 Science News Blog. It covers many disruptive technology and trends including Space, Robotics, Artificial Intelligence, Medicine, Anti-aging Biotechnology, and Nanotechnology.

Known for identifying cutting edge technologies, he is currently a Co-Founder of a startup and fundraiser for high potential early-stage companies. He is the Head of Research for Allocations for deep technology investments and an Angel Investor at Space Angels.

A frequent speaker at corporations, he has been a TEDx speaker, a Singularity University speaker and guest at numerous interviews for radio and podcasts. He is open to public speaking and advising engagements.