Fitch Ratings says in its latest Global Housing and Mortgage report that while the rate of home price increases is likely to slow in 2017, continuing government macro-prudential efforts to dampen unsustainably rapid price rises, such as mortgage lending restrictions, are being overpowered by a fundamental excess demand for home purchases.

“Home purchases in many countries continue to become increasingly expensive relative to household income and rents, driven by the combination of extremely low borrowing costs, readily available credit, steady economic growth and limited housing supply. These conditions look set to remain in place this year,” said Andrew Currie, Managing Director, Structured Finance, Fitch.

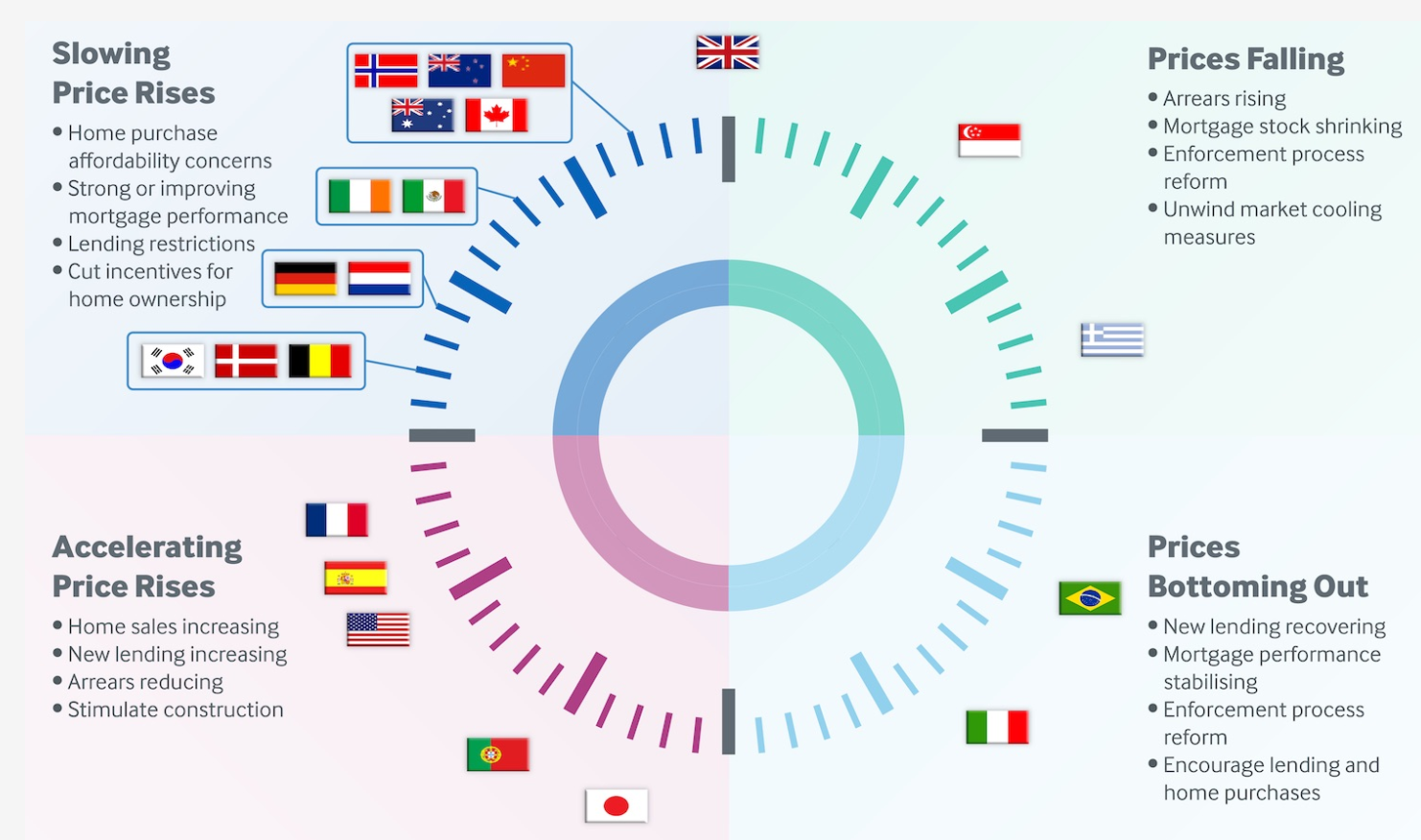

Fitch has a Stable or Stable/Positive outlook for the housing and mortgage markets for 19 of the 22 countries covered by the report. Despite this, unsustainably rapid price rises in some countries such as New Zealand, Norway and Canada are expected to moderate in 2017.

For the first time, Fitch’s report covers China’s housing market, where home prices in China’s largest cities rose by 25% in 2016 and Fitch predicts the outstanding mortgage balance in 2017 will be more than three times higher than the 2012 volume. However, in contrast to many markets, Chinese authorities directly control many aspects of housing and mortgage markets. As a result, Fitch expects 2017 price rises of only 2.5% in the largest cities, partly in response to tougher rules on home purchase and minimum loan deposits.

In North America, US home prices and delinquencies are back at 2006 levels, a decade after the subprime crisis began. Loans originated post-crisis maintain their strong performance and prices are supported by fundamentals, although some sub-markets are overheated. In Canada, household debt, reached a new high of almost 168% of disposable income in 2Q16 and, for the first time, breached 100% of GDP and is higher than the UK and US household debt burden.

There are only four markets covered by the report experiencing falling home prices and in Europe the legacy of the financial crisis continues to fade. Italian home prices are expected to stabilise after years of declines, leaving Greece as the only European country with falling prices. In the UK, Brexit-related uncertainty and stretched home purchase affordability will halt UK home price rises in 2017.

House price growth is likely to decelerate sharply in several Asia-Pacific (APAC) markets in 2017, as affordability constraints, increasing supply and tighter lending and regulatory standards dampen price dynamics, Fitch Ratings says in its latest Global Housing and Mortgage Outlook.

Fitch expects a sharp drop in China’s tier 1 city house-price growth to 2.5%, from a 25% rise in 2016 and several years of rapid price increases, partly in response to tougher rules on home purchases and minimum loan deposits. The market should also cool in other tiers, although at varying rates. However, we do not anticipate a major correction, as the Chinese authorities directly control many aspects of the housing and mortgage markets. Ongoing urbanisation, low interest rates and strong income growth will also support prices.

House price gains in Japan and South Korea are forecast to slow marginally. Aging demographics are a long-term constraint in both markets, although the 2020 Olympic games will drive Tokyo prices higher in the near-term. Oversupply and high household indebtedness in South Korea will gradually soften the market.

Singapore is the only APAC market for which we have a stable/negative outlook. An influx of new supply, slowing immigration, a soft economy and ongoing measures to cool the property market are likely to continue to dampen sentiment. However, mortgage delinquencies for the major banks should remain low – in line with the healthy labour market and strong household balance sheets, even as short-term rates rise over the next two years.

Brian Wang is a Futurist Thought Leader and a popular Science blogger with 1 million readers per month. His blog Nextbigfuture.com is ranked #1 Science News Blog. It covers many disruptive technology and trends including Space, Robotics, Artificial Intelligence, Medicine, Anti-aging Biotechnology, and Nanotechnology.

Known for identifying cutting edge technologies, he is currently a Co-Founder of a startup and fundraiser for high potential early-stage companies. He is the Head of Research for Allocations for deep technology investments and an Angel Investor at Space Angels.

A frequent speaker at corporations, he has been a TEDx speaker, a Singularity University speaker and guest at numerous interviews for radio and podcasts. He is open to public speaking and advising engagements.