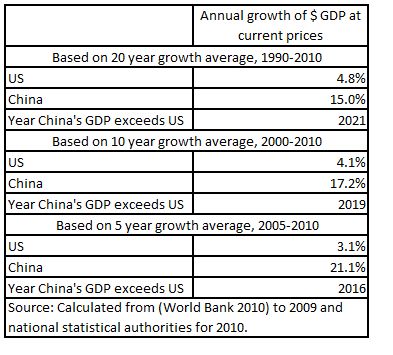

The central date for China’s GDP to overtake the US at market exchange rates is 2019 – a study of growth assumptions and analyses

Note: Why is this a topic on Nextbigfuture ? This like the the large political shifts in the middle east have a large impact as to what will happen in the future. This site is concerned with large impacts on the future, whether they are from good or bad policies, new science and technology or events. If world war 3 were to break out then it would be important to predict it and know its impact. The recent financial crisis effected what will happen in the world. The economic boom and the rise of the internet during the 1990’s effected the world.

Purchasing Power Parity

Subramanian reports that the new version of the Penn Tables, to be released in February 2011, will revise its estimate of China’s PPP up by 27 per cent (Subramanian, 2011).

Utilising such higher PPP estimates of the size of China’s GDP can give projections for when China’s GDP will overtake the US which are very short – as already noted that it has already occurred in the case of Subramanian and that it will occur in 2012 in the case of The Conference Board. It may be noted, however, that even the IMF, utilising its own lower estimates, now projects that China’s GDP will overtake the US in PPP terms shortly after 2015

Projections of a 30% move by the yuan over three years from exchange rate and inflation

Fred Bergsten, at the Peter G. Peterson Institute for International Economics, believes that there may have been a breakthrough agreement on the Chinese-US exchange rate

The real rate (chinese yuan) against the dollar is now rising at an annual rate of 10 to 12 percent, which if continued would complete the needed correction of 20 to 30 percent over two to three years, and official US reactions suggest that assurances that the adjustment will continue may have been received.

Conditions inside China are presumably the most important factor in the authorities’ decision to let the renminbi rise significantly. Inflation has replaced growth as the leading concern for economic policy and a stronger currency in a very open economy like China’s is one of the most effective instruments to counter surging prices (and for the central government to impose its will on often-recalcitrant provisional governors). Growth itself continues at near double-digit levels and, with the high probability of reasonably robust expansion in the US and world economies for 2011 and beyond, the authorities can now be confident that China will not suffer a relapse even if its trade surplus declines a bit.

We must also have no illusion that the Chinese are letting market forces determine the rate. They will continue to intervene heavily and simply manipulate it to a stronger level that is both more beneficial to their own economy and more compatible with global equilibrium. In light of the gradual pace of appreciation, and the lags of two to three years between currency moves and trade results, we must also recognize that China will continue to run sizable (if falling) external surpluses for at least another five years (and thus keep buying more Treasury bills, albeit hopefully at a declining rate).

The postulated outcome, a rise of 20 to 30 percent in the renminbi over two to three years, would have major positive effects. China’s global current account surplus would drop by $300 billion or so from the rising path that it would otherwise be on, and retreat well within the unofficial norm of 4 percent of GDP that has been discussed by the G-20 and endorsed by some Chinese officials. The US external deficit would drop by $50 billion to $100 billion, creating perhaps 500,000 new and high-paying jobs (mainly in export industries) in this country. We know that currency changes produce these powerful results because the earlier rise of the renminbi during 2005–08 and the 25 percent fall of the dollar during 2002–07, along with the global recession, produced declines (with the usual lags) of fully one half in both countries’ imbalances by 2009 (before they started rising again last year because the currency corrections halted or reversed). The world’s only major currency misalignment would be largely corrected, and the outlook for world growth and global finance would become much stronger and much more sustainable

.

It is not particularly valuable to attempt to refine the figures further to arrive at a more precise date – too many elements, with too high a degree of uncertainty, exist to try to determine whether China’s GDP will exceed that of the US in, for example, 2018 or 2020. What is significant, however, is that on any input of the range of actual comparative performance during the last twenty years China’s economy, in current exchange rate terms, will exceed the US at some point during the period 2017-2021. Furthermore such a date range is not greatly sensitive to changes in reasonable, in light of past performance, inputs.

Such a finding has a precise economic meaning. It means that some fundamental change must take place in existing trends within approximately a ten year time frame for China’s GDP at market prices not to overtake the US in the period 2017-2021.

If, as pointed out above, PPP calculations lead to excessively early projections for when China’s GDP will exceed the US, it is equally the case that projections that China’s GDP will not overtake the US at market exchange rates within the range 2017-2021 have to rely on asserting that an absolutely fundamental change will take place during the next decade. The ‘status quo’ scenario is that China’s GDP at market exchange rates will exceed the US in this period.

While, of course, a sharp change in relative inflation or exchange rates could produce a significant change in the above trends most frequently those who assert that China’s GDP will not overtake the US during the coming decade postulate a major change in relative US and China constant price growth rates. For these to prevent China’s GDP overtaking the US at market exchange rates during the next ten years it must be postulated either that a fundamental acceleration of the US economy will occur or, as few analysts predict such a development, more usually it must be asserted that for some reason a severe slowing of China’s economy during the next decade will occur.

It is perhaps due to a difficulty in accepting the reality of China overtaking the US as the world’s largest economy that there exists a large ‘catastrophist/drastic slowdown’ literature on China.17 Detailed examination of these various perspectives is beyond the scope of this paper. For present purposes it is sufficient to note that short of such a drastic slowdown in the near future, that is on the basis of continuation of the trends that have prevailed over the last decades, China’s GDP at market exchange rates will overtake the US approximately in 2017-2021.

If you liked this article, please give it a quick review on ycombinator or StumbleUpon. Thanks

Brian Wang is a Futurist Thought Leader and a popular Science blogger with 1 million readers per month. His blog Nextbigfuture.com is ranked #1 Science News Blog. It covers many disruptive technology and trends including Space, Robotics, Artificial Intelligence, Medicine, Anti-aging Biotechnology, and Nanotechnology.

Known for identifying cutting edge technologies, he is currently a Co-Founder of a startup and fundraiser for high potential early-stage companies. He is the Head of Research for Allocations for deep technology investments and an Angel Investor at Space Angels.

A frequent speaker at corporations, he has been a TEDx speaker, a Singularity University speaker and guest at numerous interviews for radio and podcasts. He is open to public speaking and advising engagements.