The Chinese currency Renminbi, or the yuan, has appreciated 34 percent against the U.S. dollar since the exchange rate reform began eight years ago. The yuan advanced some 20 percent against the euro during this period.

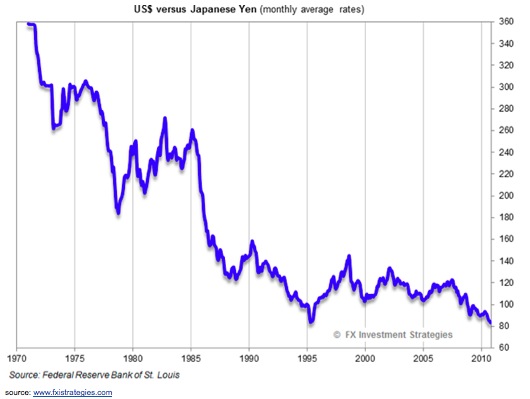

What seems likely to happen with the Chinese yuan versus the US dollar over the next 17 years and 27 years out to 2030 and 2040 ?

Headline figures show that China’s exports surged from 20% of GDP in 2001 to almost 40% in 2007, which seems to suggest not only that exports are the main driver of growth, but also that China’s economy would be hit much harder by an American downturn than it was during the previous recession in 2001.

Jonathan Anderson, an economist at UBS, a bank, has tried to estimate exports in value-added terms by stripping out imported components, and then converting the remaining domestic content into value-added terms by subtracting inputs purchased from other domestic sectors. At first glance, that second step seems odd: surely the materials which exporters buy from the rest of the economy should be included in any assessment of the importance of exports? But if purchases of domestic inputs were left in for exporters, the same thing would need to be done for all other sectors. That would make the denominator for the export ratio much bigger than GDP.

Once these adjustments are made, Mr Anderson reckons that the “true” export share is just under 10% of GDP (in 2007). That makes China slightly more exposed to exports than Japan, but nowhere near as export-led as Taiwan or Singapore.

Net exports accounted for 8.8 percent of China’s GDP in 2007, but fell to only 4 percent in 2010.

In 2013, China could be done to about 2% of GDP in net exports.

In 1958, 86% of urban workers in China were employed by state-owned firms. Between 1995 and 2001, the Communist Party laid off 46 million state-sector workers — equal to sacking the entire combined workforces of France and Italy in six years. As a result, the state’s share of urban employment fell to 28 percent in 2002, and now stands at 19 percent.

That sounds like a lot, right? But there are 1.35 billion people in China, of which approximately 795 million are in the work force in some capacity. How do 45 million Chinese workers – manual laborers, for the most part, working in companies that operate on Foxconn’s margins – produce $1 out of every $3 in China, as the share of GDP from export sales would indicate ? They don’t.

Why? Because the export/GDP ratio didn’t discount the imported materials (“churn”). It just lumps everything into “exports,” regardless of where the materials actually came from. These “made in China” goods actually have very little in them that was made domestically in China.

China is shifting to ramping up domestic consumption. This will mean a stronger currency would be helpful.

China’s shift to domestic consumption means that a stronger currency will mean citizens will be able to import oil and commodities at lower

Jim Rogers was a partner of George Soros. Jim has a net worth of over $300 million. He wrote books predicting the boom in commodity prices since the 1990s and has been a China bull since at least 1984.

Compared to the yuan’s value in 2005 (when it was 8.3 to 1 US $), Rogers expects it to appreciate by as much as 500 percent in the future. This would be about 1.7 to 1 US$.

If the Chinese yuan appreciated 350% from the 2005 level or about 250% from current levels that would put it at 2.4 to 1 US$. If China’s GDP doubles from GDP growth of 6% per year over 12 years and also increases by 250% from currency appreciation, then this would be a 5 times increase in GDP from 2013 to 42 trillion GDP in about 2025.

5 years of 4.5% GDP growth would add about 25% to China’s GDP which would make it about 53 trillion in 2030. This would put in the general range of the Standard Chartered projection for 2030.

My project is that China will be in the US$40-80 trillion GDP range in 2030 and most likely in the 50 to 70 trillion GDP range.

I think India’s and Brazil’s economy will lag relative to the projection below.

If you liked this article, please give it a quick review on ycombinator or StumbleUpon. Thanks

Brian Wang is a Futurist Thought Leader and a popular Science blogger with 1 million readers per month. His blog Nextbigfuture.com is ranked #1 Science News Blog. It covers many disruptive technology and trends including Space, Robotics, Artificial Intelligence, Medicine, Anti-aging Biotechnology, and Nanotechnology.

Known for identifying cutting edge technologies, he is currently a Co-Founder of a startup and fundraiser for high potential early-stage companies. He is the Head of Research for Allocations for deep technology investments and an Angel Investor at Space Angels.

A frequent speaker at corporations, he has been a TEDx speaker, a Singularity University speaker and guest at numerous interviews for radio and podcasts. He is open to public speaking and advising engagements.