Nextbigfuture just covered the bankruptcies hitting solar and coal companies as China changes its energy mix. China is shifting to more efficient coal power and a smaller coal industry.

Weak world economic growth seems likely to continue for 5-10 years.

China’s biggest coal producer by volume — China Shenhua Energy Co Ltd, which has vowed to focus on clean-coal production, renewable energy and nuclear power to address the national shift of consumption-driven economy, according to its Chairman Steve Zhang Yuzhuo.

The coal producer expects renewable energy output to account for more than 20 percent of profits by 2025 as it plans to become a leading clean-energy provider.

Such transformational moves come as China plans to increase the share of non-fossil energy to 15 percent by 2020 and 20 percent by 2030, as well as capping coal’s contribution to total energy consumption at 62 percent within five years.

Coal accounted for 64 percent of energy use last year, down 4.5 percentage points from 2012, when supply gluts and weak demand led to a drop in coal prices.

This means long term pressure on solar power and coal companies. Solar because of increased supply and competition and low energy prices and coal because of less demand

Energy and economic experts had predicted that low oil prices would kill US Shale oil producers. There has been a hit to the Shale producers but they are getting more efficient and have lowered the oil price where they can breakeven.

Other less efficient oil producing countries like Venezuela have taken a bigger hit.

- China could make their coal plants 50% more efficient (from 33% to 50% thermal efficiency)

- China will continue to have weaker growth in the 4-7% annual range

- China will shift to 20-25% power from renewables and nuclear power

Oil prices will stay pretty low to very low

The shale industry is unlike any other conventional hydrocarbon or alternative energy sector, in that it shares a growth trajectory far more similar to that of Silicon Valley’s tech firms. In less than a decade, U.S. shale oil revenues have soared, from nearly zero to more than $70 billion annually (even after accounting for the recent price plunge). Such growth is 600 percent greater than that experienced by America’s heavily subsidized solar industry over the same period

The transition to Shale 2.0 will take the following steps:

1. Oil from Shale 1.0 will be sold from the oversupply currently filling up storage tanks.

2. More oil will be unleashed from the surplus of shale wells already drilled but not in production.

3. Companies will “high-grade” shale assets, replacing older techniques with the newest, most productive technologies

in the richest parts of the fields.

4. As the shale industry begins to embrace big-data analytics, Shale 2.0 begins.

Technological progress in big data analytics could create Shale 2.0 and bring US oil costs to $5-20 per barrel.

Incremental and dramatic improvements will continue in all aspects of the many technologies used in shale production: logistics, planning, seismic imaging, well-spacing, fluid and sand handling, chemistry, drilling speed, pumping efficiency, instrumentation, sensors, and high-power lasers. Shale fields will increasingly be developed using advanced automation, mobile computing, robotics, and industrial drones. At present, barely 10 percent of projects use fully automated drilling and pressure-control systems, for example.

Big Data can make oil fracking 4 times more efficient

Many companies are keeping their big-data projects proprietary, some information is publicly available. Halliburton reports that its analytic tools achieved a 40 percent reduction in the cost of delivering a barrel of oil. Baker Hughes says that analytics have helped it double output in older wells.

At present, each long horizontal well is typically stimulated in 24–36 stages, with, on average, only one-fourth to one-third of those stages productive. At present, in other words, about 20 percent of stages generate 80 percent of output.

The current state of stimulation technology means that, on average, at least 300–400 percent more oil is not extracted. Bringing analytics to bear on the complexities of shale geology, geophysics, stimulation, and operations to optimize the production process would potentially double the number of effective stages—thereby doubling output per well and cutting the cost of oil in half.

In late 2015, China’s cabinet said they would try to cut pollution from coal-fired power plants by 60 percent by 2020 through upgrades to plants, according to a report by Xinhua, the state news agency. If successful, the plan for upgrades would reduce carbon dioxide emissions from such plants by 180 million metric tons, the report said.

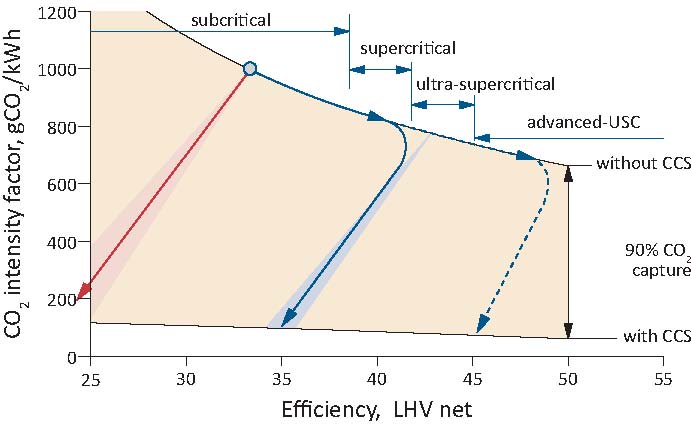

Upgrading existing plants and building new high-efficiency, low-emissions (HELE) coal-fired power plants addresses climate change concerns in two important ways. In the near term, emissions can be reduced by upgrading existing plants or building new HELE plants. Such plants emit almost 20% less CO2 than a subcritical unit operating at a similar load. Over the longer term, HELE plants can further facilitate emission reductions because coal-fired plants operating at the highest efficiencies are also the most appropriate option for CCS retrofit.

The best new coal plants in China are in the Ultra-supercritical 44-46% efficiency range.

Developments in AUSC steam cycles are expected to continue this trend. AUSC coal-fired plants are designed with an inlet steam temperature to the turbine of 700–760°C. Average metal temperatures of the final superheater and final reheater could be higher, up to about 815°C. Nickel-based alloy materials are needed to meet this demanding requirement. Various research programs are underway to develop AUSC plants. If successful, a commercial AUSC-based plant would be expected to achieve efficiencies in the range of 45–52% (LHV [net], hard coal). A plant operating at 48% efficiency (HHV) would emit up to 28% less CO2 than a subcritical plant, and up to 10% less than a corresponding USC plant. Commercial AUSC plants could be widely available by 2025, with the first units coming online in the near future.

Ultracritical coal reactor turbines in China

Brian Wang is a Futurist Thought Leader and a popular Science blogger with 1 million readers per month. His blog Nextbigfuture.com is ranked #1 Science News Blog. It covers many disruptive technology and trends including Space, Robotics, Artificial Intelligence, Medicine, Anti-aging Biotechnology, and Nanotechnology.

Known for identifying cutting edge technologies, he is currently a Co-Founder of a startup and fundraiser for high potential early-stage companies. He is the Head of Research for Allocations for deep technology investments and an Angel Investor at Space Angels.

A frequent speaker at corporations, he has been a TEDx speaker, a Singularity University speaker and guest at numerous interviews for radio and podcasts. He is open to public speaking and advising engagements.