Bad debts in the Chinese banking system are ten times higher than officially admitted, and rescue costs could reach a third of GDP within two years if the authorities let the crisis fester, Fitch Ratings has warned.

China debt and banking problem is described at the Telegraph UK from a Fitch Ratings report

The agency said the rate of non-performing loans (NPLs) has reached between 15pc and 21pc and is rising fast as the country delays serious reform, relying instead on a fresh burst of credit to put off the day of reckoning.

It would cost up to $2.1 trillion to clean up this toxic legacy even if the state acted today, and much of this would inevitably land in the lap of the government.

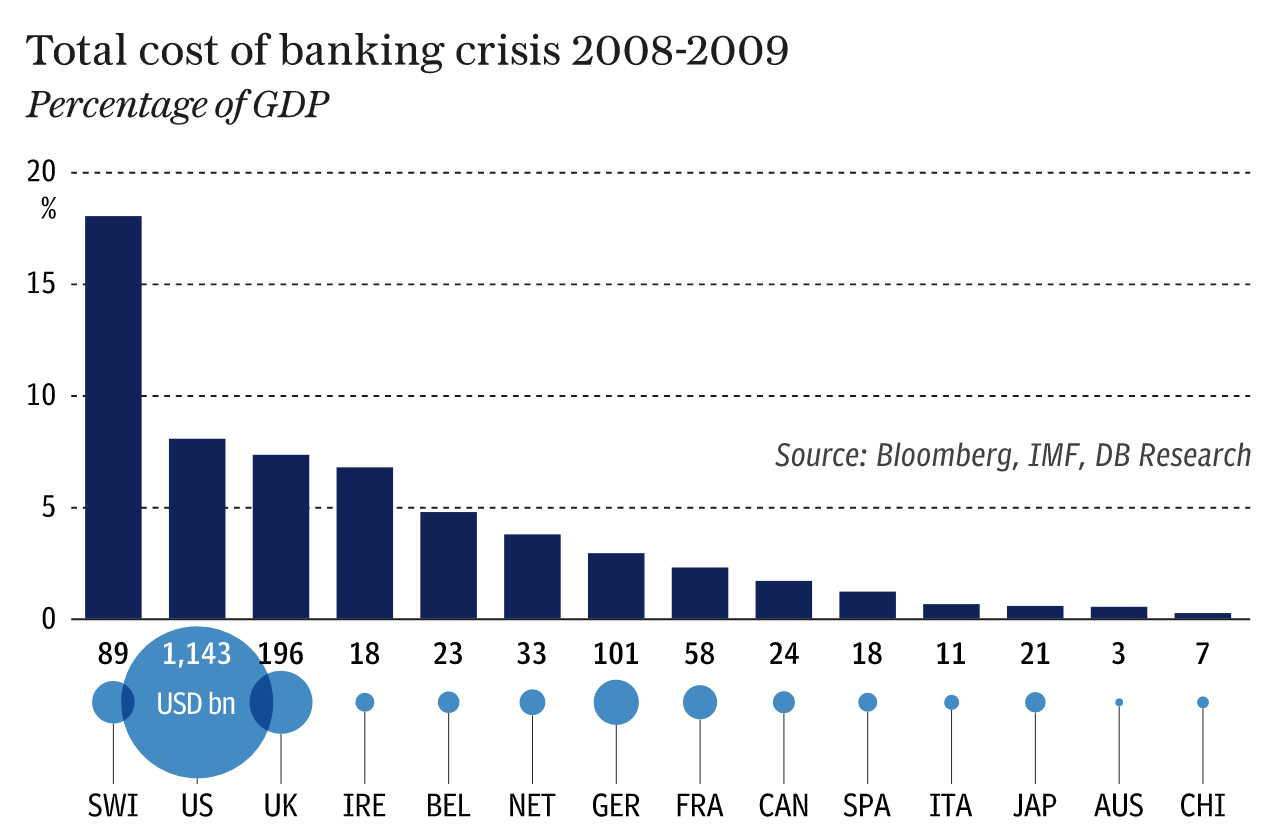

The damage eclipses losses during the global financial crisis in Britain and the US, where the direct costs of bank rescues were roughly 8pc of GDP. It would be closer to the trauma suffered by Ireland, Greece, and Cyprus when their banking systems collapsed, but on a vastly greater scale.

Michael Pettis has been looking at China’s debt situation for many years. Pettis says, “The conclusion is inexorable. Beijing must find a way of generating domestic demand without causing China’s debt burden to surge, which basically means it must rebalance the economy with much faster household income growth than it has managed in the recent past, and it must begin aggressively writing down overvalued assets and bad debt to the tune of as much as 25-50% of GDP without causing financial distress costs to soar. Everything else is just froth.

Pettis calculated that if we believe debt is equal to 240% of GDP, and is growing at 15-16% annually, and that debt-servicing capacity is growing at the same speed as GDP (6.5-7.0%), for China to reach the point at which debt-servicing costs rise in line with debt-servicing capacity Beijing’s reforms must deliver an improvement in productivity that either:

Causes each unit of new debt to generate more than 5-7 times as much GDP growth as it does now, or

Causes all of the assets backed by the total stock of debt (which we assume to be equal to 240% of GDP) to generate 25-35% more GDP growth than they do now.

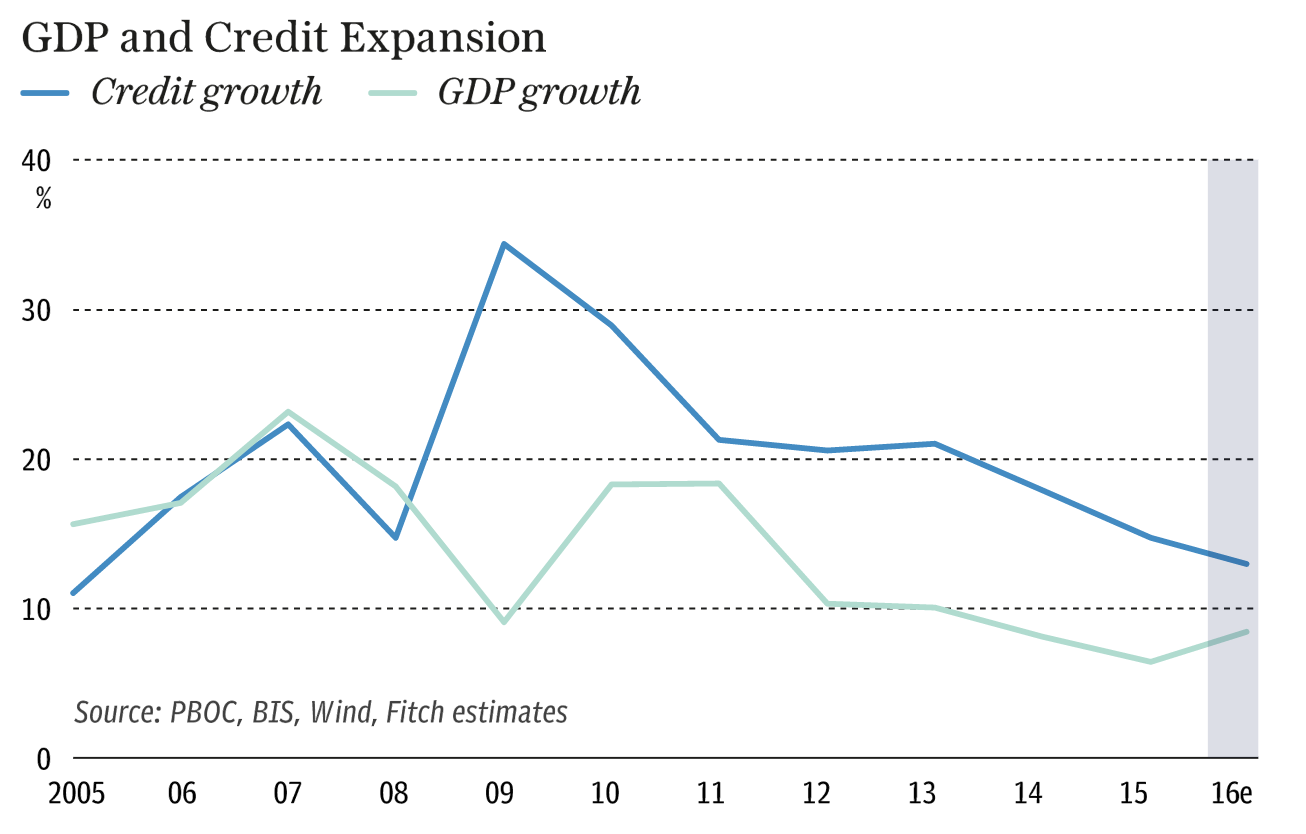

Credit reached 243pc of GDP by the end on last year, double the level in 2008. Banking system assets have grown by $21 trillion over that time, 1.3 times greater than the entire US commercial banking nexus.

Fitch estimates that the ratio will jump to 253pc this year, and 261pc next year.

The credit addiction is becoming increasingly dangerous for two reasons. The efficiency of credit has collapsed. Fitch estimates that each new yuan of credit generates just 0.3 yuan of economic growth, down from 0.8 before the Lehman crisis.

“We think the Chinese authorities can still clear this debt,” said Mark Williams from Capital Economics. “In an extreme scenario – with non-recoverable loans of 25pc – we calculate that the government would have to spend a full 35pc of GDP bailing out the banks. That would lift debt to 90pc. That is high but in principle it is possible.”

Mr Williams said it will be very hard for Beijing to repeat the tricks used to overcome the last banking crisis in the late 1990s. A roaring global boom – and surging nominal GDP – whittled down the burden of state’s bail-out bonds, and the use of “financial repression” to hold down deposit rates for effectively imposed the cost on savers.

Neither are now possible. Deposit rates have been liberalized. The global context is entirely different and China is starting to face demographic strains from a shrinking work force. Mr Williams said the biggest worry that the Communist Party fails to deliver on reforms, leading to economic stagnation and a darkening calculus for the debt trajectory. “We’re afraid that growth could drop to 2pc,” he said.

Brian Wang is a Futurist Thought Leader and a popular Science blogger with 1 million readers per month. His blog Nextbigfuture.com is ranked #1 Science News Blog. It covers many disruptive technology and trends including Space, Robotics, Artificial Intelligence, Medicine, Anti-aging Biotechnology, and Nanotechnology.

Known for identifying cutting edge technologies, he is currently a Co-Founder of a startup and fundraiser for high potential early-stage companies. He is the Head of Research for Allocations for deep technology investments and an Angel Investor at Space Angels.

A frequent speaker at corporations, he has been a TEDx speaker, a Singularity University speaker and guest at numerous interviews for radio and podcasts. He is open to public speaking and advising engagements.