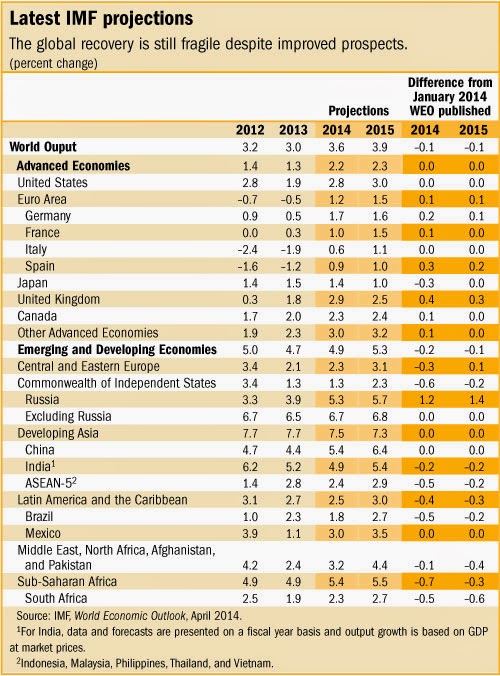

The IMF forecasts global growth to average 3.6 percent in 2014―up from 3 percent in 2013―and to rise to 3.9 percent in 2015.

The global recovery is becoming broader, but the changing external environment poses new challenges to emerging market and developing economies, says the IMF’s latest World Economic Outlook (WEO).

“The recovery which was starting to take hold in October is becoming not only stronger, but also broader,” said IMF Chief Economist Olivier Blanchard. “Although we are far short of a full recovery, the normalization of monetary policy—both conventional and unconventional—is now on the agenda.”

Blanchard cautioned, however, that while acute risks have decreased, risks have not disappeared.

In this setting, the global economy is still fragile despite improved prospects, and important risks—both old and new—remain. Risks identified previously include finishing the financial sector reform agenda, high debt levels in many countries, stubbornly high unemployment, and concerns about emerging markets.

The 234 page IMF 2014 World Economic Outlook report.

Emerging markets and developing economies

• Emerging market and developing economies continue to contribute more than two-thirds of global growth, and their growth is projected to increase moderately from 4.7 percent in 2013 to 4.9 percent in 2014 and 5.3 percent in 2015. The weaker momentum compared with advanced economies reflects in part the adjustment to a less favorable external financial environment and, in some cases, continued weak investment and other domestic structural constraints. Going forward, stronger exports to advanced economies are expected to underpin moderate increase in growth.

• The forecast for China is that growth will remain broadly unchanged at about 7½ percent in 2014–15 as the authorities seek to put the economy on a more balanced and sustainable growth path. In India, real GDP growth is projected to strengthen, partly due to government efforts to revive investment growth.

• Only a modest acceleration in activity is expected for regional growth in Latin America, with growth rising from 2½ percent in 2014 to 3 percent in 2015). Some economies have recently faced strong market pressure.

• In sub-Saharan Africa, growth continues at a strong pace, and is expected to increase from 4.8 percent in 2013 to 5½ percent in 2014–15. Commodity-related projects elsewhere in the region are expected to support higher growth.

• The Middle East and North Africa face challenging conditions, with regional growth projected to rise only moderately in 2014–15. Most of the recovery is due to the oil-exporting economies, while many oil-importing economies continue to struggle with difficult sociopolitical and security conditions.

• Near-term prospects in Russia and many other economies of the Commonwealth of Independent States (CIS) have been downgraded, reflecting the fallout from the Ukraine crisis. In emerging and developing Europe, growth is expected to decelerate in 2014 before recovering moderately in 2015, largely reflecting changing external financial conditions.

Key downside risks

The WEO notes that the balance of risks to global growth has improved, but that some hurdles along the way remain. These include the following:

Danger of low inflation. The report reiterates the risk from persistently low inflation in advanced economies, especially in the euro area. Inflation is projected to remain below target for some time, as growth is not expected to be high enough for economic slack to decline rapidly. Longer-term inflation expectations are then more likely to drift down in response, and risks of lower-than-expected inflation, or even deflation, will increase, because interest rates are already close to zero and only limited options remain for using monetary policy to respond. The result would be premature increases in the cost of borrowing and higher real debt burden. The lingering danger is that the longer inflation remains weak, the more vulnerable the region is to damaging debt deflation in the event of adverse shocks to activity.

Emerging market risk. Tighter financial conditions and the resulting higher cost of capital could lead to a larger-than-projected slowdown in investment and durables consumption in emerging markets, and thereby weigh on growth. The potential for reversal in capital flows from emerging markets to advanced economies as risk averse investors seek relatively more attractive advanced economies’ assets remains another concern. And there is a risk of renewed bouts of market volatility with the expected normalization to a more neutral monetary policy stance in the United States. In either case, the result could likely lead to financial turmoil and difficult adjustments in some emerging markets, with a risk of contagion.

Geopolitical risks. Recent developments in Ukraine have increased geopolitical risks. Greater spillovers to activity beyond neighboring trading partners could emerge if further turmoil leads to a renewed bout of increased risk aversion in global financial markets, or from disruptions to trade and finance from intensified sanctions and counter-sanctions.

If you liked this article, please give it a quick review on ycombinator or StumbleUpon. Thanks

Brian Wang is a Futurist Thought Leader and a popular Science blogger with 1 million readers per month. His blog Nextbigfuture.com is ranked #1 Science News Blog. It covers many disruptive technology and trends including Space, Robotics, Artificial Intelligence, Medicine, Anti-aging Biotechnology, and Nanotechnology.

Known for identifying cutting edge technologies, he is currently a Co-Founder of a startup and fundraiser for high potential early-stage companies. He is the Head of Research for Allocations for deep technology investments and an Angel Investor at Space Angels.

A frequent speaker at corporations, he has been a TEDx speaker, a Singularity University speaker and guest at numerous interviews for radio and podcasts. He is open to public speaking and advising engagements.